How does one retire early in New Zealand?

On this site you will read a lot of advice about savings, FIRE, reducing the costs of your car and your groceries and starting side hustles, but how does this all lead to early retirement?

The reality is – money is messy.

Many people have no idea where their money is, where it goes, and how much they have.

Even when they reach a retirement-level of net worth, most are unsure how to turn their assets into a money-making machine that will allow them to live comfortably without working.

For example:

Let’s say you’re a diligent saver, you’ve contributed to your Kiwisaver like a good boy/girl for your entire career, you’ve paid off your mortgage, and now your assets look like this:

This is great, but if you’re not financially educated, seeing this will just give you anxiety.

Will I run out of money?

How do I get my money out?

How much can I spend?

What if I lose it all?

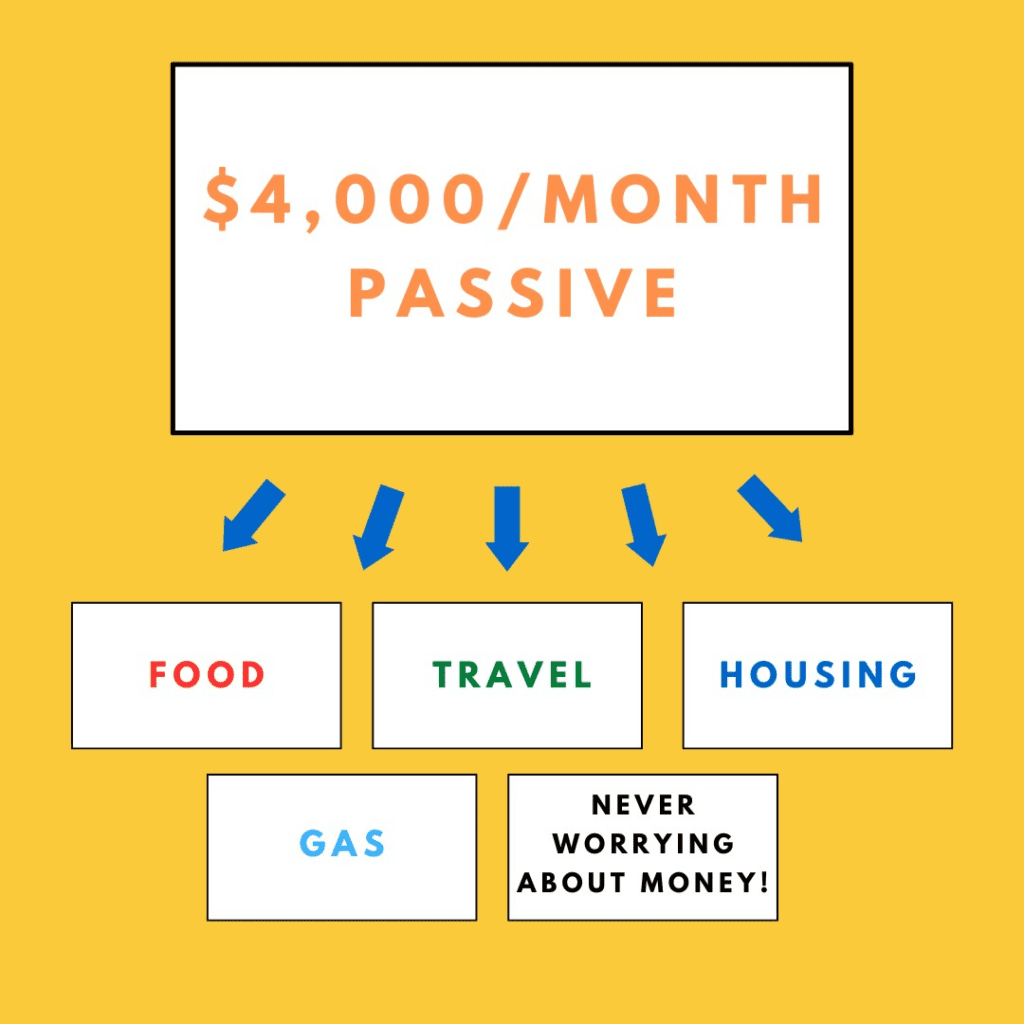

What you really want is to take all those assets, and set them up so you have this:

Believe it or not, the two graphics above show exactly the same thing.

Show them to any financial planner, and they will see two identical pictures.

The large amount of assets equals the $4,000/mth passive income, and vice versa.

So how do we get from the first picture to the second picture?

You just need to understand how a few simple truths about how money works.

Then early retirement will make all the sense in the world, and you’ll know exactly how to get there.

The Big Picture Of Early Retirement

Say you want to live on $50,000 per year.

If you have a net worth of $1 million, you will be withdrawing 5% of your cash every year.

Some simple math will tell you – you’ll run out of money after 20 years.

But here’s the thing – that $1 million doesn’t just stay as $1 million.

If it’s sitting in the bank, it will be earning interest.

If your bank account is earning 2% interest over the long term on average, you will earn at least $20,000 in interest per year.

This means in the first year you will need to withdraw $30,000, to get your $50,000 in spending money for the year.

The following year you will earn slightly less interest (since you withdrew $30k, bringing your savings balance down to $970k), meaning you will need to withdraw slightly more.

With some simple math, we can see that we will run out of money after 28 years:

Now – if you’re 65, that’s probably not such a bad situation. You’re set until 93, if you live that long, and the reality is you won’t actually run out of money, because you’ll also be getting about 20k per year in pensions.

However, if we’re aged 35, the story is different.

We don’t get a pension for another 30 years, and we need our money to last much longer.

Thankfully, that’s not difficult to do.

We just need to ensure our money isn’t just sitting in the bank earning 2%, but is sitting somewhere else earning much more.

The reality is, most people don’t retire this way anyway. This was just a numerical example to help you understand the equation.

During retirement, most people will have their money invested, so it continues to work for them.

To keep things simple, let’s say you’ve managed to grow your net worth to $1 million by paying off a $500,000 house and you have $500,000 in index funds.

The stock market (NZX 50) has returned about 10% per year over the last 30 years (excluding dividends), and pays around a 2.8% dividend each year. Inflation target for NZ is 1-3% per year.

So let’s assume the following:

- Living costs of $40,000 per year, increasing by 2% inflation per year.

- NZX 50 will return 8% p.a. on average.

- We get a 2.5% annual dividend.

How long would our $500k last?

You can see that after 30 years, we haven’t lost any money.

In fact, we actually got richer every year.

Our $500k in stocks has grown to $923k, despite selling some stock to make withdrawals every year.

The simple explanation is – even though we sell some stock to pay our living expenses, the stock that remains goes up in value.

Since we’re withdrawing around 6%, but our stocks are returning 8%, we never run out of money.

We also get an annual dividend, which means you don’t have to sell that much in the first place.

Also, small changes matter.

If we decide we want to live on $50k per year (a 20% increase), the entire equation changes:

You can see we will deplete our entire $500k in savings after 22 years.

However, even this isn’t a disaster situation, because remember – you still have your $500k house!

And the reality is, this $500k house has now probably grown to $1m+ over that 22 years.

You can simply sell your house and do the same thing all over again (not to mention, you’ll be getting a pension once you hit $65).

And of course, if this is cutting it too close to the line for you, you always have the option to simply spend less.

Bring your spending down from $50k to $40k, or $3,333 per month, and you will never run out money.

In fact, you’ll continue to get richer every year.

What About My House?

This is a big issue for many New Zealanders.

Many are millionaires, but their entire net worth is tied up in their homes.

As I’ve said before – a house that you live in is not actually an asset, but a liability.

The reason is – it doesn’t produce any income, but produces a lot of expenses.

So what do you do with your home when you reach your FIRE number?

You can:

- Sell the house and start renting.

- Rent the house out and start renting.

- Sell the house, buy a smaller house, invest the difference

- Continue living in the house, live off other investments.

The first 3 options are self-explanatory, and you will simply employ the maths that we worked out in the earlier examples.

The final option requires you to have other liquid investments to live off. Therefore, if you have a $1m house, your FIRE number will likely be closer to $1.5m.

In any case, try to remember that unless your house produces income, it’s not an asset. If early retirement is your goal, it’s much wiser to buy a smaller house and put your cash towards other cash-flowing assets.

What If The Stock Market Crashes?

The stock market crashes all the time, but it’s never permanent.

What you should understand is the stock market is a direct reflection of our economy.

For you to lose all your money, it would mean the NZX 50 would need to crash and go to zero.

What that would mean is all of these companies are now bankrupt:

- Air NZ

- Auckland Airport

- Fletcher Building

- Spark

- The Warehouse

- Mainfreight

- Contact Energy

- Mercury Energy

- Meridian Energy

- Briscoes

- Port of Tauranga

Not only that, if the NZX 50 were at zero, it would mean there are literally no other public companies in New Zealand.

In other words, New Zealand would basically need to stop existing.

Is that possible?

Sure, I guess.

How possible is it?

I’m guessing a probability of 0.000000000000000001%.

Probably not odds you need to spend much time worrying about.

If we do ever go through a bear market, you could mitigate your “losses” by spending slightly less in those years. That would mean you won’t need to sell as much stock at bear market prices, and you’ll reap the benefit in the eventual recovery.

The True Secret To Early Retirement

I’ve been retired for a few years now in my thirties, and the secret is not losing sight of the big picture.

Nothing changes during retirement, except you can now relax.

However, your spending habits should still remain the same.

That means you should:

- Keep living within your means

- Keep investing any money you do get

- Keep busy

- Keep to your plan!

In the forecasts we did earlier, I budgeted for $40,000 in annual living costs, or $3,333 per month.

However, that’s more than anyone should need to live comfortably, even in NZ.

To be honest, I personally struggle to spend that much per year.

Even as I write this, I’m travelling, splurging on an apartment that is far too big and nice for me, which is costing me around $1,800 per month. I spend around $100/week on food, and maybe $40/week on Ubers. My day is made of things like reading, walking, going to the gym, running, surfing, sports, cooking, or working on something I enjoy (like this website).

I’m spending around $2,500 – $3,000 per month, and my portfolio often grows by significantly more than that, meaning even in retirement, my net worth continues to increase.

Now if I were leasing a Ferrari, living in 5-star hotels and flying business class, my money would be gone before I’m 40.

Thankfully, I have no need for any of that (and neither do you or anyone else!)

In the end, retiring early is just about being financially responsible until you get there, and staying financially responsible once you are there.

Do that right, and you’ll never need to worry about money ever again.