Aussie retail stocks have been very interesting over the past twelve months.

Many are at multi-year lows – not surprising – the market prices in rising rates and the coming recession that the news likes to talk about every day.

However, many are priced so low you’d think rather than a “possible recession”, it’s more like Australia is already deep into a multi-year depression with no way out.

One example was MYER – a stock I wrote about last year – trading so low it was practically free at one point, even though it had almost half a billion cash in the bank.

It has since recovered strongly once the market woke up, but what about the rest of the sector?

In this article I’ll delve into one cash-generating machine I think the market may have underpriced, and how it compares to the wider industry.

A Forgotten IPO

Dusk IPO’d near the end of 2020.

The news then was dominated by lockdowns and vaccine rollouts, so the IPO was practically a secret. Nobody was interested in a homewares retailer going public when most Australians couldn’t even leave their house, let alone go to the shopping mall and buy small luxuries.

What people missed was a highly profitable niche retailer that’s been around since 1999, with an impressive track record of both sales and profit growth.

The first thing that came to mind when reading the Dusk annual report was an anecdote from Warren Buffett, who often talked about the power of businesses that don’t require large amounts of capital.

His example is always See’s Candies, which requires practically no capital but generates large amounts of cash.

When Buffett bought See’s Candies, it had the following numbers:

- $30 million per year in sales

- $2 million in profit

- $8 million of net assets.

In other words, the business required only $8 million in assets to generate $2 million in profit each year.

A return on capital of 25%.

Compare this to something like a REIT, which also makes $2 million in (cash) profit, but requires something like $40 to $50 million in assets.

Sometimes the line of thinking goes – look at this company with such a big amount of valuable assets! What a great company to own!

But, especially in inflationary times, large capital requirements are a detriment because capital (assets) need to be replaced, and inflation makes that very expensive. The ability to generate large amounts of cash with very little capital is a huge advantage.

Buffett ended up acquiring See’s Candies for $25 million, and it has since produced over $2 billion in profits.

Who would have thought Buffett, with all his multi-billion dollar investments in banks and insurance companies and railroads, would make his best returns selling peanut brittle and chocolate?

Often it’s the simple business that works best.

This brings me to Dusk (DSK:ASX)

Dusk’s core business is candles.

It doesn’t cost much to make a candle. You need a wick (basically string) and some wax. You need some scents. Then you need to make them look nice. Pretty much it.

Today Dusk’s numbers are as follows:

- $139 million in sales

- $18.5 million in profit

- $36.5 million in net assets.

Quick math on that is a return on capital of 51%.

To paint a fuller picture of how little capital it needs, it’s also sitting on $21 million in cash and no debt. It carries only $11 million of actual fixed assets – most of its balance sheet is made up of leases, which is its main operational cost, and even that isn’t large.

The other wonderful thing about the candle business – it’s a consumable.

It runs out, and every few weeks you have to buy another one.

Of course, not every household buys candles (just like not every household buys peanut brittle), but the ones that do will most likely be repeat customers.

High-margin product, repeat customers, and almost no capital required to produce it….

Is this another See’s Candies?

Sales

Dusk has only been listed for two years, but in their prospectus, we have (unaudited) data from 2017.

Sales have grown from $65 million to $138 million since 2017 – a CAGR of around 16% on sales for the past six years (including three years of a pandemic).

However, maybe the most promising part is their gross margins, which they have maintained above 65% very comfortably.

Gross margins that high are almost never sustainable, because they attract competition quickly. It’s extremely easy for someone to start up a similar business next door and undercut you, especially when barriers to entry are not high (candles are not hard to make).

There are only two ways a business maintains gross margins that high for that many years – either you’re a monopoly, or you have an extremely strong brand and customer loyalty. And obviously Dusk isn’t a monopoly.

Where Is The Growth From?

Growth in retail comes from two places: Same stores and new stores.

Obviously, you can’t keep opening new stores forever, so ideally you want to see growth from both your old stores and new stores.

Then once you’ve saturated all your locations, you want a business that simply gushes cash once new store growth stops (think supermarkets, fast food).

Dusk is currently in a heavy growth phase, opening around 10 stores per year, and has just expanded into its first international market (New Zealand).

We can see Dusk had strong LFL (like-for-like) sales growth, or same-store growth up until FY2022. Dusk claims they lost 24% of trading days in the first half of 2022, which would explain the decrease.

This will be a key metric to keep an eye on in FY2023 to see if the growth story has recovered.

However, the fact that Dusk still managed to open ten new stores during the year is a testament to the resilience of their business model in probably the toughest retail environment Australia has seen in my lifetime.

How is this possible?

The key – once again – is in their tiny requirements for capital.

It does not cost Dusk much to open a new store.

In fact, here is an insight from their prospectus:

What this means is Dusk only spends $105,000 on a new store opening, and the store typically produces $281,000 in operating profit on average within the first twelve months.

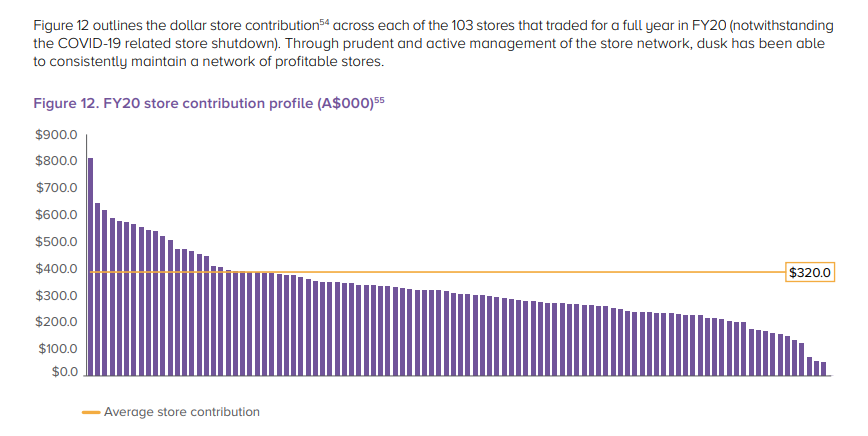

Here’s is that broken down in more detail:

We can see the current stores produce on average $320,000 each year (Dusk defines “contribution” as gross profit less operating costs per store).

To the left of the graph, we see some stores bring in up to $600,000 per year (the $800,000 per year store is most likely the online store).

To the right, you can see even their least profitable stores produce $100,000 in contribution per year.

As each store only requires $105,000 to open, this means every new store is completely paid back within twelve months, including lower-earning stores in suburban areas and B and C-grade malls.

As of September 2022, Dusk confirms that every single store is profitable:

Again, this is the advantage of a low capital model.

Dusk makes $18 million in profit per year, and opening a new store only costs them $105,000. This means it is extremely low risk and they can expand rapidly – the only bottleneck to their expansion is the market itself.

However, this does leave us with two questions:

- How many stores can Dusk micro-manage? None are franchised, all are fully owned. Can they grow “too fast”?

- At what point do they saturate the market and diminishing returns on new stores set in? (for example, two stores in the same suburb). We know the Australian market is profitable, but this might not be the case overseas when they are forced to expand to new markets.

We do have some foresight on how this might play out.

The prospectus stated the goal was to have 160 stores by 2024. That would mean an additional 28 stores to be opened in 2023 and 2024. It’s looking like they will probably fall slightly short of that goal, as they’re currently opening around 10 stores per year.

Early in FY23, Dusk also opened three stores in New Zealand.

When they first made the announcement of NZ stores in planning, I’d assumed the major malls like Sylvia Park, Britomart, Newmarket to be the top contenders, so when the stores finally opened I found the locations interesting – Manukau City Westfield, Northwest Shopping Centre Massey, and Queensgate Shopping Centre Wellington.

However, it makes sense upon re-reading the prospectus:

Personally, I am not a big fan of retail in New Zealand – in my breakdown of NZ’s major retailers, it was clear most of them don’t make a lot of money, margins are not good, and the ones that do make money are making most of it in Australia.

Therefore, I am equally cautious on this market for Dusk. Personally, I would have preferred them to just continue focusing on Australia. I don’t expect Dusk’s New Zealand business to contribute much to the bottom line, retailers simply don’t make much money in NZ. However, the management has also said they will use New Zealand as a test dummy for new strategies and new markets.

Maybe it will be a net positive. Wait and see.

Product Mix

Dusk is more than candles.

Here is the breakdown from their prospectus:

And here is an updated product mix from their H1 2023 results:

Candles have been consistent in making up between 30% to 40% of the sales mix. The next biggest segment is diffusers, while gifts, homewares and mood reeds make up the majority of the remainder.

This differentiation in products is useful, as after talking to various candle fans, it’s quite clear that people have strong preferences for diffusers vs candles vs mood reeds. Dusk covering the full range of home fragrances, while still maintaining a reasonably specialised niche, means they hit all customers.

The Dusk Experience

When I was in Australia earlier in the year I had the chance to visit a Dusk store.

I spent about 15 minutes chatting with the sales girl who told me the following:

- The busiest day of the year is easily Boxing Day, followed by Xmas Eve.

- Valentine’s Day and Mother’s Day are also strong (but not as big as Boxing or Xmas Eve).

- There’s not really a “best seller”, people buy a big range of things.

Dusk has talked often about its new “Glow 2.0” store layout, which to me looked nice enough, though nothing particularly impressive that I noticed. However, it is probably quite an upgrade to their Legacy layout:

The thing that caught my eye, however, were the prices.

Candles are not cheap!

So this becomes a lesson on how to sell a block of wax for $50.

Firstly, the store is positioned as a gift store. So much of the store is focused on presentation, such as packaging, colours and lighting.

It makes gift shopping extremely easy.

Finally, the candles are branded very smartly.

It’s not a strawberry candle, it’s an Acapulco – Guava & Strawberry 2-Wick.

The marketing is quite brilliant.

I won’t buy a $50 candle for myself, but would I buy a guava and strawberry candle for someone else?

Absolutely!

The business model is fully integrated, meaning Dusk designs the candle and formulates in-house, it’s manufactured overseas by a third party, then it’s retailed exclusively by Dusk in Dusk-only stores. Most candles can be bought in other boutique and gift stores, but if you want a Dusk candle, it can only be bought at a Dusk store.

Here’s the other interesting thing I found:

Candles are addictive.

Let me explain.

In the name of market research, I did end up buying a $50 candle for myself.

Actually, I bought two, because it was a 2-for-1 special, and I couldn’t decide on a single flavour.

I made sure to light it every night while I was working.

After about a week, it’s a habit.

Sitting at my desk for more than five minutes feels strange if I don’t have guava and strawberry scents filling my room and a flame flickering on my desk.

When the wick finally ran out and I was left with a big useless blob of wax, my first instinct was to stop working and go and buy a new candle so I could start working again.

Of course, I did not go and buy a new candle, because I’ve read too many books on marketing and was able to resist this Jedi mind trick.

However, now I completely understand how Dusk has managed to sign up 750,000 loyalty members who buy candles regularly, and how candles and scents have become a half a billion dollar industry in Australia.

Let’s talk cash flow

Many of you know I focus more on cash flow than any other metric.

Here’s how Dusk holds up:

Obviously, we need to look at this in the context of Covid, which started around March 2020 (Q4 of FY20).

When Dusk produced a stellar result in FY21 (mostly because online sales boomed for many retailers while everyone was staying at home, apparently in candlelit rooms), most chalked it up to them being a rare beneficiary of Covid.

However, a closer look at the data shows that wasn’t really the case. For Dusk, online sales increased marginally during FY21, but most products were still bought in-store:

Cash flow dipped heavily in FY22, which was expected as this was the lockdown year (Melbourne had 200 days of lockdown, almost all of it in FY22 (July 2021 to June 2022). Dusk also stated in their annual report they lost 24% of all store trading days during the first half of FY22 due to lockdown.

In this context, it’s hard to normalise their free cash flow level. Probably the best guess we can make is to look at FCF per store:

This was growing comfortably until FY21, but I think a reasonable estimate is Dusk should be able to hold $100,000 per store reasonably comfortably (depending on the success of the NZ stores).

Dusk has already opened 3 new NZ stores and 5 new Australian stores in the first half of FY23, with plans to open at least 3 more in Australia in the second half.

At a forecasted store count of 143 stores to end FY23, I think we could reasonably see free-cash-flow of at least $14m to $15m.

After their recent 1H23 results release, we can gauge whether they are on track to meet this.

We can see in they managed to do $17.7m in free cash flow in the first half:

The interesting thing about retail is they usually generate most of their profit in the first half. This is because H1 includes the Christmas period, and H2 is when many bills become due and get paid.

Therefore it’s not unusual for them to actually be FCF negative in the second half, or generate very little.

For example, note the following trend:

FCF 2021

1H: $21.36m

Full year: $17.16m

Difference: 19%

FCF 2022

1H: $18.48m

Full year: $12.89m

Difference: 30%

So as a guesstimate, we can assume full year FCF will be between 19% to 30% lower than H1.

That would put us between 12.39m to $14.34m.

Valuation

Now that we have free cash flow, we can estimate a valuation:

To be prudent, we’ll take $12.39m as their forecasted FCF for 2023.

As a conservative estimate, we’ll assume they don’t grow at all for the next 10 years, and just keep on generating $12.39m in FCF per year.

As an optimistic estimate, we’ll give a reasonably modest growth rate of 10% per year for 5 years, falling to 5% per year for the next 5 years.

At today’s price, even a conservative estimate (which is very conservative) will give you a valuation of $2.52 and margin of safety of 33%. Our optimistic estimate gives us a share value of $3.78 and a margin of safety of 55%.

Keep in mind your risk is further reduced as their capital requirements are tiny and they have zero debt with $33m in cash in the bank. As I like to say, it’s very difficult to go bankrupt when you don’t owe anybody money, and doubly hard when your business requires very little capital.

Talking multiples, at today’s price Dusk has a market cap of $104m, with $33m of net cash gives them an Enterprise Value of $71m.

With annual free cash flow of $12.39m, you’re looking at a multiple of 5.7x.

As as sweetener, you get an 8% to 10% annual dividend while you sit and wait.

Risks

To me the biggest risk right now is management risk.

Peter King is the current CEO but will be standing down in late 2023. He has been with the company through its entire growth phase and has done a tremendous job.

CEO changeovers are always a business risk, much like changing the coach of a Superbowl winning team or perhaps the star quarterback.

As always, you have competition risk as well, although this is less concerning to me. As I mentioned earlier, Dusk being able to maintain 60% gross margins for almost a decade proves that the homewares market has strong brand loyalty, and as they grow I expect them to sustain this. Their 700k paying subscribers is a testament to this. While the candle market does not have strong barriers to entry, to produce at scale and compete with established brands does not make this an easily challenged market. Management believes the market currently is worth around half a billion AUD, and should grow between 5% to 10% per year.

The third major risk I see is supply chain risk, as Dusk currently outsources all its manufacturing. Most are from China, though there are some other players too:

As Covid showed, global shipping reliability can change overnight. Dusk did prove that its model is resilient, staying very profitable through the entire pandemic, but of course overseas relationship always carries the risk of disruptions.

Finally, in a rising interest rate environment and possible recession, luxuries are the first products to fall. Will people stop buying birthday and mother’s day gifts in a deep recession? Yes, probably. Will profits go down? Probably. However, as I said, Dusk in insulated from interest rate risk due to their debt-free status, and their business model is incredibly lean and nimble. They do not require big up-front investments to open stores, and stores completely pay back their investment within a year. This makes them uniquely suited to adapt to changing environments, and if store closures are necessary, assuming the store has been open at least a year, they can be done without suffering any permanent loss. Again, as they are debt free, as long as they can simply break even during a tough trading period, they should be able to trade through it just fine.