When investing, I’m always looking for ways to preserve capital.

That means rather than trying to make a lot of money, I’m trying to make sure I don’t lose a lot of money.

The way this translates to stocks is – I try to look for a stock that is very unlikely to go down a lot.

To achieve this you need two things.

- You need a company with very good/reliable assets

- You need a company trading for a very cheap price

For example, imagine you have a company that owns $10 million in farmland.

As we know, farmland is very valuable and is not going out of fashion any time soon.

As long as humans continue to eat food, we will continue to need farmland.

Now imagine this company is currently trading on the stock market at a market value of $20 million.

This means we are buying $10 million in farmland for $20 million.

Farmland is a great asset, but we’re paying too much for it in this scenario.

However, what if the company is trading for a market value of $5 million?

Now, we’re buying $10 million in farmland for $5 million.

Great deal.

Assuming land values don’t crash 50% (which doesn’t happen often), we’re getting $5 million in farmland for free.

Even if land values do crash by 50%, our farmland will drop in value from $10 million to $5 million, and we bought it for $5 million, meaning we didn’t actually lose any money.

In investing, we call this buffer a margin of safety.

If you look hard enough, you can find deals like this in the stock market all the time.

Keep this idea in mind as we go through this next stock.

The idea

Today we’re looking at NZ hotel operator Millennium & Copthorne Hotels.

Here’s what first nudged me to look into this company:

I was looking for NZ companies being priced at less than book value.

This means; companies where you could buy $1 of assets for 50 cents (like our farmland example).

MCK came up as a candidate. Here’s what it looks like on the surface:

It has a market cap of $347m.

It has net assets of $514m.

Translation: We are buying $514m of assets for $347m.

Looks like it could be a bargain.

So what’s the next step?

We want to make sure we are not buying junk assets (for example, some little tech business they bought for $500m but doesn’t actually make any money).

Let’s deep dive into their annual accounts and take a look at exactly what we’re buying.

One thing you should understand before we get started – MCK owns 66% of another NZ listed company, CDL Investments (CDI).

CDI is a property development company that buys sections, develops them and sells them off.

So when investing in MCK you’re really buying two distinct businesses – the core MCK hotel business, plus 66% of CDI’s property trading business.

A preliminary look at the accounts gives this general overview of their assets:

Cash (after subtracting all debts): $108m

Hotel properties: $246m

Development properties: $152m

Investment properties: $15m

Inventories and receivables: $15m

Outstanding leases: -$15m

Total net assets: $520m1

(I had to do a bit of tricky accounting to work out these figures, to account for the 66% CDI ownership. See the footnote at the bottom).

To me, these all look like potentially high-quality assets.

Let’s dig down further and check what we’re actually buying here.

Hotel assets:

MCK owns 14 hotels:

Queenstown: 3

Auckland, Rotorua: 2 each

Te Anau, Greymouth, Dunedin, New Plymouth, Wellington, Palmerston North: 1 each

Bay of Islands: 49% of 1.

They also have 3 franchised hotels in Taupo, Wairarapa and Wanganui.

Plus two managed hotels in Auckland and Paihia.

(Managed and franchised hotels means they don’t own the property, but they earn revenue from either franchise royalties, or managing the hotel and receiving a management fee).

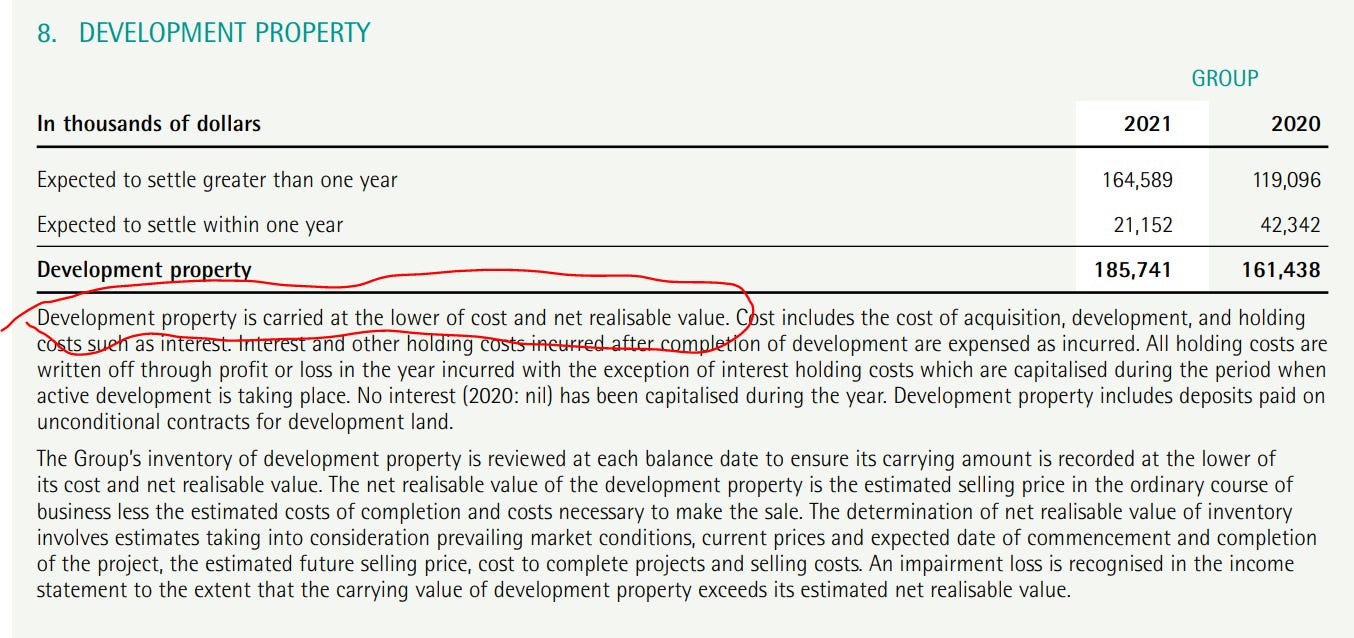

Development properties:

Almost all property development assets are owned by MCK’s subsidiary, CDL Investments NZ, of which it owns 66%.

I don’t have a breakdown of what each development site is worth, but we do know the total cost of the sites was approximately $209m:

As MCK owns 66% of this, their stake is worth approximately $138m.

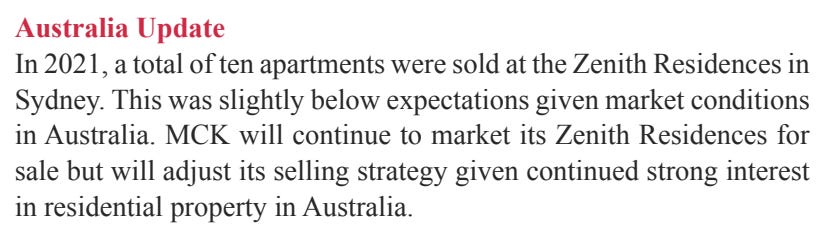

Australia properties:

MCK also owns a small apartment complex in Sydney called Zenith Residences which it is in the process of developing and selling, currently valued at $29m.

So to recap, we are buying the following:

14 hotels worth ~$246m

6 development sites and an apartment complex worth ~$167m

Cash of ~$108m (after all liabilities paid)

That’s a total of $520m in net assets, and we can buy it today for $347m.

Looks pretty good right?

The hidden value in MCK

There’s a kicker here that reveals even more value in MCK.

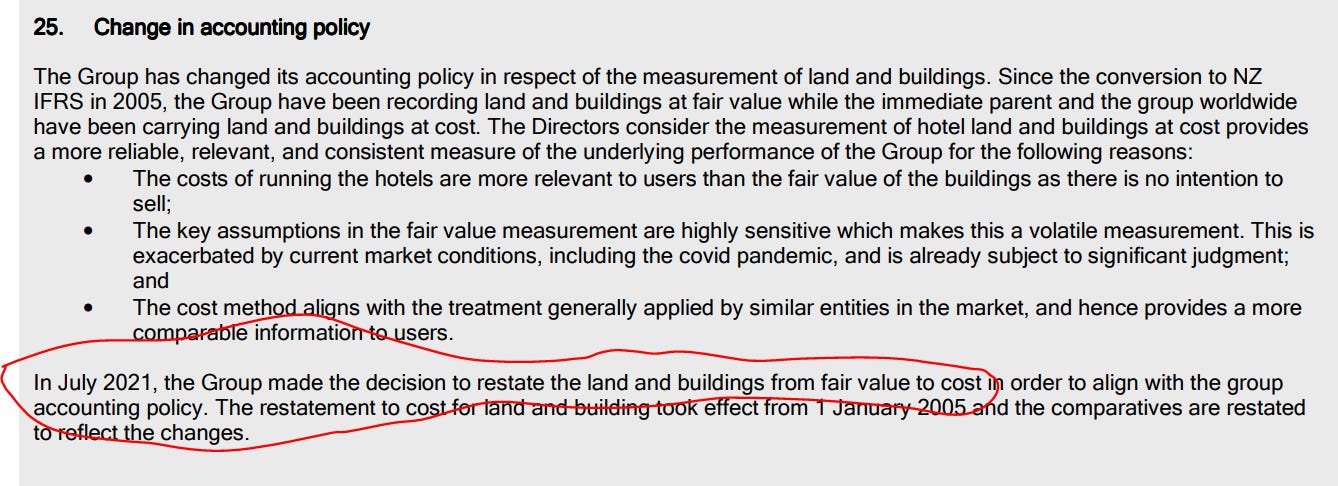

In the MCK and CDI annual reports, there’s a little clause that people might skip over.

MCK annual report:

CDI annual report:

In July 2021, the Group made the decision to restate the land and buildings from fair value to cost…

If you’re not from an accounting background this may not mean anything, so I’ll try to explain.

There is a choice in accounting to state your assets at either:

- Cost (how much you paid for it), or

- Fair value (how much you could realistically sell it for today).

There are good arguments for both approaches, but properties are generally valued at fair value, since properties are generally easy to sell at any time if you need to.

However, the annual accounts reveal MCK and CDI both state their property values at cost.

This means the figure we see in their accounts is the amount they paid for it, not the market value.

This is like your mother buying a house in 1960 in Ponsonby for $70,000, and thinking her house is still worth $70,000.

Of course, this is wrong, we all know property values go up over time, so today her house is probably worth a couple million.

Let’s go back to how this applies to MCK.

We concluded they own hotels worth $246m, and development and investment properties worth $167m.

However, now we also know that is not the market value, that is the cost (how much they paid for it).

How much are they actually worth today?

Well, they’ve told us that too.

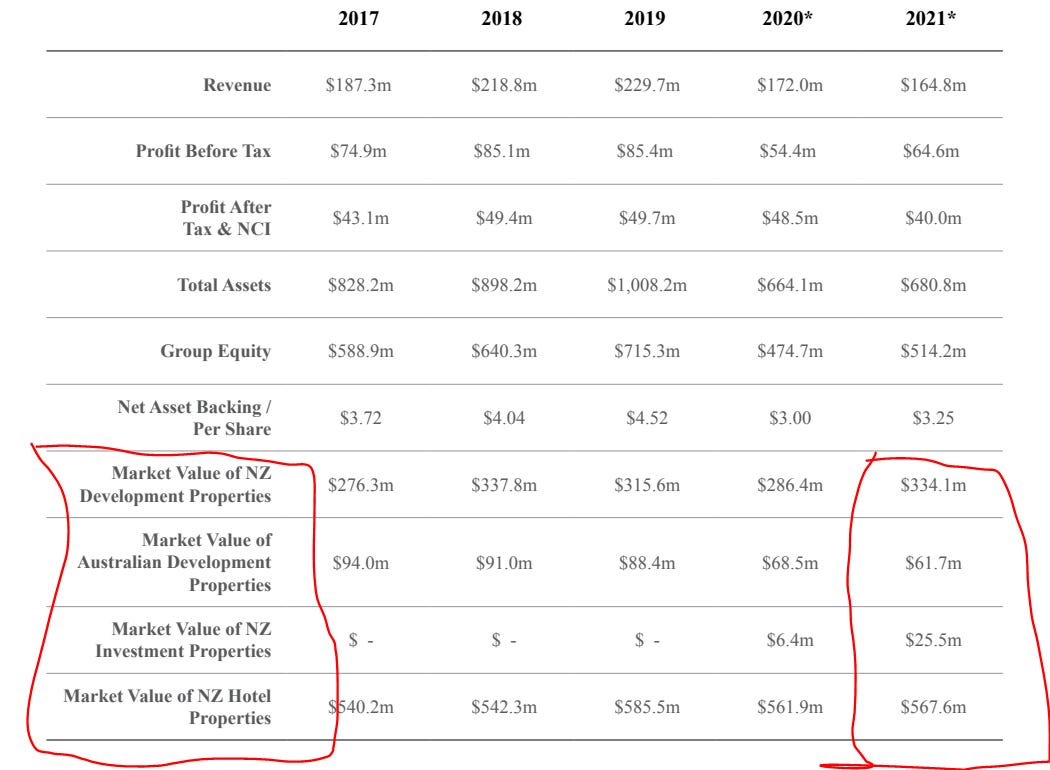

This is MCK:

This is CDI:

Let me simplify this:

CDI has development properties recorded at cost of $165m, but the market value is $334m (of which MCK owns 66%)

CDI has investment properties recorded at cost of $23m, but the market value is $25m (of which MCK owns 66%).

MCK has hotel properties recorded at cost of $245m, but the market value is $568m.

The assets are worth a lot more than we initially thought.

I had to do another round of tricky accounting to figure out these totals, but here’s what MCK’s stake looks like by my calculations at market value:

14 hotels worth ~$568m

6 NZ development sites and an Australian apartment complex worth ~$299m

Cash of ~$108m (after all debts paid)

That’s a total of $975m in assets, and we can buy it today for $347m.

Don’t forget about the business!

Remember, we’re not just buying properties that sit there and do nothing.

MCK is a business!

So when we buy this stock, we get the business as well.

That sounds like a good thing, but it’s not necessarily. If the business is shitty and making lots of losses, this means things might not look as good.

If the business is great and makes a profit, that would make things look even better.

Let’s find out.

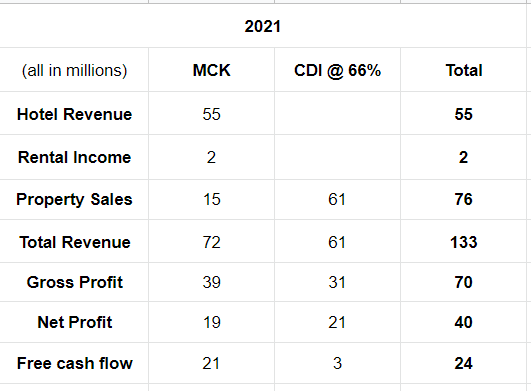

Again, a bit of accounting is required to work out the “true” MCK stake, since the annual report mixes MCK and CDI together, but here’s what I came up with after crunching the numbers for 2021:

There’s also some hidden value here because 2021 was a horrendous year for travel and the pandemic is not a recurring event.

We can assume that eventually, travel will normalise, meaning their hotel business should also normalise.

What does their “normalised” business look like?

We can figure that out by looking at their accounts pre-pandemic.

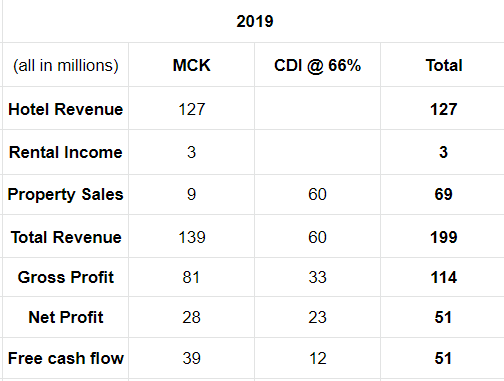

Here’s what their numbers were from 2019:

That might just look like a stack of meaningless numbers to some of you, so here’s a quick summary:

In 2021 the company generated around $24m in free cashflow per year.

At today’s share price, they have an EV (Enterprise value) of $239m, giving them a free cashflow yield of 10x.

(This means the business takes 10 years to generate what we paid for it).

By most comparisons that’s a very stable business and not expensive from a multiples perspective.

However, if we use their free cashflow figures from before the pandemic, they actually generate $51m in free cashflow per year.

That would give them a free cashflow yield of around 4.5x, which I would consider very good value.

Their gross margins are above 50% which is very healthy.

41% of their revenue is hotel revenue.

57% of their revenue is property sales.

2% is rental.

It’s reasonably well-diversified.

Even pre-pandemic, hotel revenue was only 64% of revenue, so still well diversified.

Will business normalise post-pandemic?

Common sense says it should, but it might take longer than one expects. Overall it’s a resilient business which is profitable and margins are healthy.

The history and current ownership

This is quite an interesting story and took a while to get my head around.

Millennium Copthorne’s origins go back to a company called Euro National, run by the infamous Rod Petricivic, which went public in 1985.

The share price crashed from $8.20 to 87 cents in the 1987 crash.

Much of the tumble was due to its poor investments, one of which was Kupe Investments, which it owned 47.5% of.

In 1992, a Singapore hotel conglomerate called CDL Hotels Intl took over Euro National, merged its NZ hotel operations into the company, and renamed the company Millennium Copthorne NZ (MCK) in 2006.

When they took over Euro National, they also got Kupe, since Euro National owned Kupe. Kupe was renamed to CDL Investments NZ, which is now a property development company listed on the NZX, and Millennium Copthorne owns 66%.

So, this is how we got to today, with MCK as a hotel company, owning 66% of CDI.

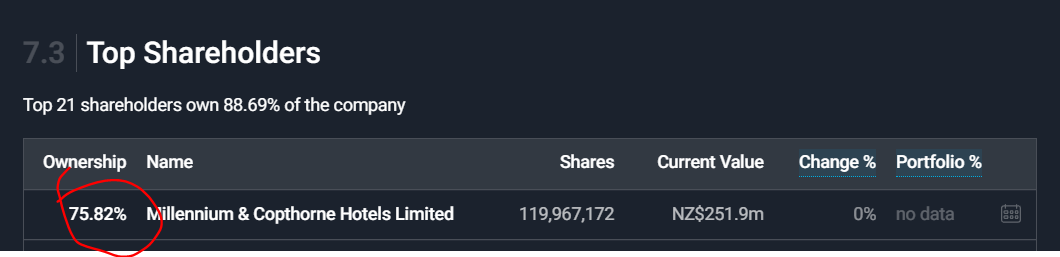

But who owns MCK?

75.82% of it is owned by Millennium and Copthorne Hotels Limited.

(note this is a different company to Millennium and Copthorne Hotels New Zealand Limited, which is the stock we’re looking at).

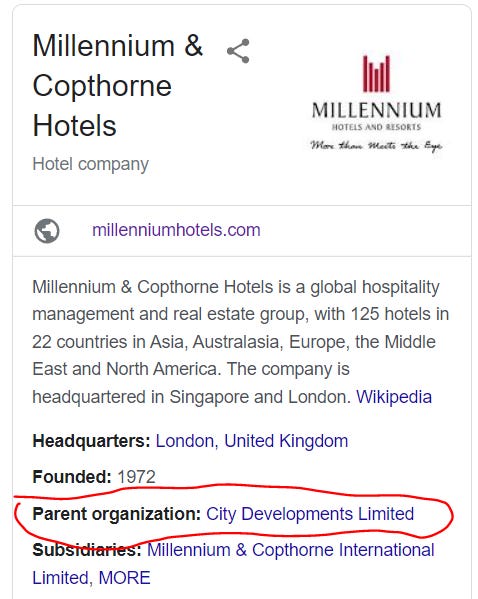

And who owns Millennium & Copthorne Hotels Limited?

They’re fully owned by a company called City Developments Limited, which is a $7 billion company listed on the Singporean stock exchange.

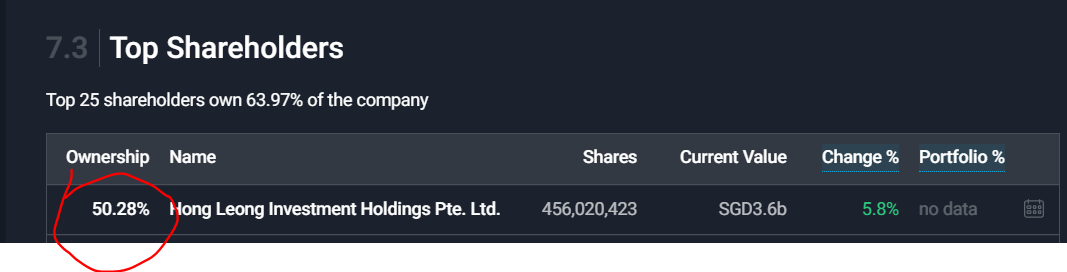

And who owns City Developments Limited?

It’s majority-owned by the Hong Leong conglomerate, which is basically a huge family empire based in Malaysia and Singapore, run by Kwek Leng Beng and Quek Leng Chan, two cousins who are also two of Asia’s richest billionaires.

So it looks like this:

CDI NZ is owned by MCK NZ.

MCK NZ is owned by MCK International.

MCK International is owned by City Developments (a Singaporean conglomerate).

City Developments is owned by Hong Leong Holdings (a Singaporean family empire).

I’ll explain why this could be important in the final section below.

My final thoughts

What attracts me to this investment is the extremely low risk of downside.

Once again, I’m much more interested in not losing money than I am in making a lot of money.

Here we have a business on sale for $347m.

However, the company has $108m in cash, so really we’re only paying $239m.

What do we get for that $239m?

We get $868m worth of properties, plus a business that generates $24m in cash per year (in a bad year).

Not to mention:

- They have no bank or interest-bearing debt, so it’s near impossible to go bankrupt.

- They are a hotel business which stayed profitable throughout one of the most devastating two years for travel in our lifetimes (covid), so we know the business is resilient.

- They pay a dividend, meaning we’re getting cash back as shareholders regularly.

- Over the last 10 years they’ve grown the stock price from 40 cents to $2.10 (and a high of $3.35), so they have shown growth potential.

I find the likelihood of losing money on this investment to be very low to almost impossible (keyword: almost).

One thing I should mention:

Of the $975m in properties (market value) we get with this investment, we saw that $567m is hotel properties.

That might look nice, but that $567m number is irrelevant in a lot of ways.

MCK isn’t planning on selling those hotel properties, so that value is likely never going to be recognised.

One advantage of them having a high market value on those properties is a source of collateral. They can borrow a large amount against the properties to fund other projects.

However, MCK doesn’t have a history of borrowing against their hotels, and haven’t mentioned any plans to start.

So even though it looks nice to be buying $567m of hotels for a fat discount, it doesn’t mean we’re about to see hundreds of millions in dividends coming down the line from property sales.

Pretty much the only benefit you get as a shareholder from this huge disconnect between cost and market value is it protects your downside.

With almost $1b of properties on the books, bankruptcy is practically impossible. We are not going to be losing money over the long term.

So, everything looks great with MCK. We’re basically getting half a billion in property for free, they’re debt-free and making millions in cash flow every year. What’s the catch?

Here is the only significant risk that I see:

We saw the company is 75% owned by a Singaporean conglomerate.

This means as a shareholder, your vote is essentially worthless. Whatever the Hong Leong family want to do with the company, they can do without your vote, since they own the majority vote.

Is that a big risk?

Probably not, but maybe.

Since all shareholders are equal, and there are laws that stop them from just straight up embezzling everything, they can’t just disappear with your money.

If they decide to sell all the properties and wind up the business, you’ll get paid, and if they decide they want money now and pay everything out as dividends, you’ll get paid too, etc.

You just have to make peace with the fact you get no say in how the company is run, and have faith they’ll run it well.

The follow-on risk is that your company is essentially owned directly by CDL Singapore. What happens if CDL Singapore and Millennium Copthorne International start getting into solvency trouble?

They’ll need to sell assets. Yes, your assets.

Again, not very likely. These companies are run by one of the most successful families in the history of Asian business, and you don’t become one of the most successful families in Asian business by running companies into the ground.

But the ownership situation is still something you need to consider.

Finally, the liquidity on the stock is terrible. When I started building a position, getting any more than a few hundred shares at a time was near impossible.

When it comes time to sell your stock (if you ever want to) you’ll probably be dealing with the same liquidity issue.

Is it a buy?

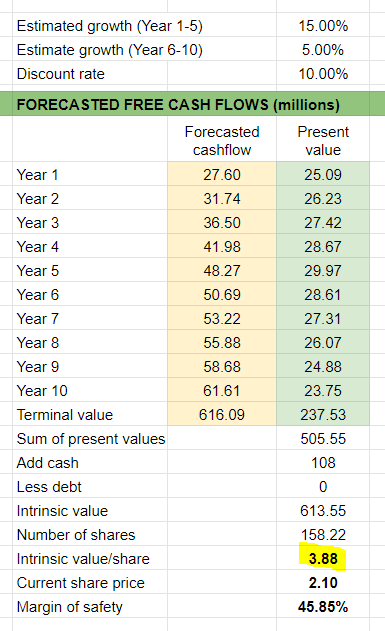

Let’s look at valuation.

This is at very conservative growth rates, assuming they only normalise to $50m free cash flow five years from now:

Overall I’ve never been a huge fan of the hotel business, but a 45% margin of safety based on cashflow, and a 65% margin of safety based on asset value, the value on MCK looks too good to ignore.

When you run the numbers with properties at cost, it’s already a solid buy.

When you run the numbers with properties at fair value, it’s practically a no-brainer for me.

$1b in assets for $347m.

$25m to $50m free cashflow.

Dividend.

Hard to go wrong.

I am a buyer all the way up to $2.70.

Disclaimer: The numbers and information in this piece are not audited and may be inaccurate. Always do your own research. Investing contains risk and you can lose money. Before you invest your money, you should seek financial advice. This article is not financial advice and I am not your financial advisor. This article is for entertainment purposes only. You are advised to read it under the assumption that I am not very smart and am probably wrong all of the time. Disclosure: Long MCK

References:

CDL Investments Annual Report 2021

CDL Investments Annual Report 2019

These numbers differ from the MCK annual report, due to MCK consolidating 100% of its CDI subsidiary into the accounts, then netting out the portion they don’t own in the equity section. Since it only owns 66% of CDI, some tricky accounting was necessary to work out the “true” ownership of assets you have as a shareholder. In short, I had to pull up the CDI annual report, use that to subtract all the CDI figures from the MCK annual report to get the “true” MCK figures. Then I had to add back 66% of the CDI figures to get the “true” amount MCK shareholders own (MCK + 66% of CDI). It also looks like my math worked out a little bit off, since the annual report shows the net assets to be $514m, and my calc came out at $520m. So just understand these numbers are probably not 1,000% correct.