Retail is a fantastic sector for small-time investors, especially in New Zealand.

- You’re probably familiar with the product/service.

- You can easily do in-person research on their business/products.

- It’s an easy business model to understand.

That third point is a big one. A lot of industries such as tech, banking, insurance, manufacturing can be hard to get your head around in terms of how a company actually makes money. Retail is a straightforward business. Most of us have probably worked a retail job at some point, seen how inventory comes in and out, seen money going through the till, seen the effects of seasonality, and all of us interact with the retail sector in our everyday lives.

This familiarity with the business model gives you a much easier time of analysing a retailer as an investment.

Let’s break down some of the things we want to look for.

Sales

Sales refers to how much money they take in at the till.

Ideally we want this to be growing on both a same-store basis (individual stores are improving sales year-on-year) and also on total basis (they’ve been opening new stores).

Gross Profit

Possibly the most important metric in retail – this refers to the profit made on the actual products themselves. If we sell a shirt for $10, and it costs $6 to make/buy, our gross profit on each shirt is $4.

Of course we’ll have other expenses like rent and wages, but those aren’t factored into gross profit. Gross profit only considers the profit on the actual product.

Having strong gross margins is vital to success in retail, because that’s where the ability to make sustainable profits and hold a competitive advantage lies.

It also indicates you have a moat of some sort – either a brand that commands a price premium, or a very high quality product others can’t match (think Nike, Rolex etc).

Free cash flow

Free cash flow is a key indicator of a healthy retail business. The nature of retail usually means you are buying large amounts of inventory at a time. If you can’t turn that inventory into cash quickly you run into:

- Liquidity problems – with all your cash tied up in inventory, you may have trouble paying bills. This leads to debt, which can spiral into more cash flow problems.

- Obsolescence – if you don’t move inventory fast enough it can become obsolete, which means it needs to be sold at discount or discarded. We saw an example of how damaging this can be recently with A2 Milk.

- Inventory costs – inventory is expensive; you need to store it, sort it, insure it, transport it. Turning your inventory over at a fast rate avoids pileup and reduces costs.

Efficiency

The last thing I look for in a retail business is efficiency. I like my retail businesses to be lean – this means being ruthless in closing down unprofitable stores, turning over inventory quickly, and adapting to trends quickly such as e-commerce, changing store fitouts and being adept at social media.

In summary, we want a company with:

- Consistent sales growth over a long time.

- Healthy gross margins (ideally above 50%) maintained over a long time.

- High inventory turnover.

- Strong free cash flow and little reliance on debt.

Currently New Zealand has five major listed retailers – Kathmandu, Briscoes, Hallensteins, The Warehouse and Michael Hill.

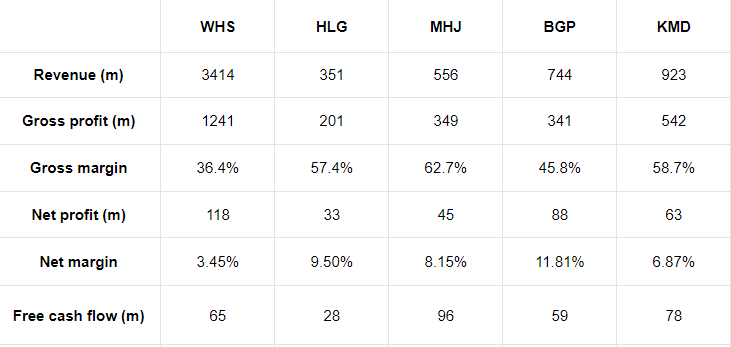

Let’s look at some numbers:

This already paints an interesting picture:

Some initial thoughts:

- The Warehouse is clearly the biggest of the five and does more in sales ($3.4b) than the other four combined.

- The Warehouse has the worst margins (not surprising for a discount retailer). Net profit margin of 3.54% is razor thin and doesn’t leave a lot of room for hiccups.

- Of the four smaller retailers, Briscoes has the lowest gross margins but the highest net margins. This means they don’t make as much profit on the products themselves, but actually make more money overall. This indicates excellent cost control – a sign of a good management team.

- Warehouse does $2.7 billion more in sales than Briscoes, but only makes $30m more in profit ($118m vs $88m), and generates almost the same free cash flow.

- Michael Hill and Kathmandu generate more free cash than The Warehouse, even though the Warehouse does 7x more sales than Michael Hill and 3.5x more sales than Kathmandu.

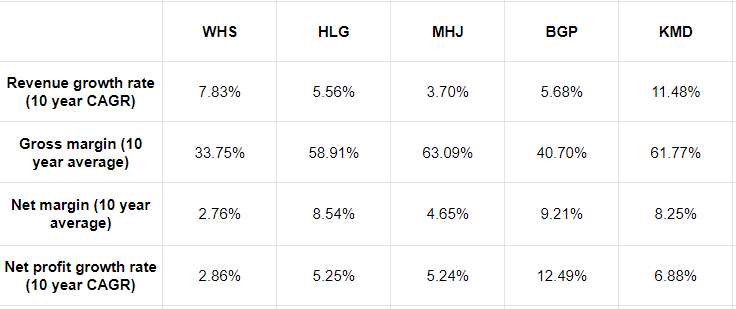

Let’s add in some historical data for context:

This isn’t telling me anything new margins wise, but it does show me they’re all growing revenue and net profit at single digit rates over ten years (low single digits once you factor in inflation) bar a couple of exceptions.

None are strongly growing retailers, which could be due to saturation, overseas competition, low growth industries, or a combination of factors (we’ll look into it later).

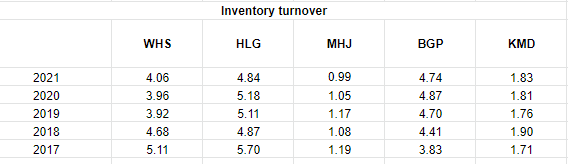

Let’s look at inventory.

We want inventory to move fast. A helpful metric here is inventory turnover.

Inventory turnover tells us how many times over they sell their holding inventory during the year. For example, if they move $5m of inventory during the year, and they hold on average $1m of inventory at any one time, their inventory turnover will be 5x.

As a general rule, higher is always better.

I’m looking for two things specifically:

First, I want inventory turnover to be consistent. If it’s improving that’s a bonus, but the main thing is that it’s maintained. If it’s going down that’s a problem.

Second, it should be at a sufficient level to make sure inventory doesn’t become obsolete. For a company like Hallensteins, whose products are very seasonal, you would want it to be above 4x. For a company like Michael Hill, where diamonds and necklaces aren’t necessarily seasonal and don’t become obsolete easily, anything above 1x could be considered healthy.

All look reasonably healthy to me.

The one I’d look into further is Michael Hill, which has room for improvement and is maybe trending in the wrong direction.

I also would have expected Warehouse to be higher, as they do sell a lot of groceries, low-cost items, fast fashion and consumables, but their numbers still look okay.

Now that we have a general picture of how each compare to each other, let’s dive in to each individually:

The Warehouse Group (WHS)

The Warehouse is a discount retailer that operates five distinct businesses:

- The Warehouse (discount everything store)

- Warehouse Stationery (stationery and electronics)

- Noel Leeming (electronics and appliances)

- Torpedo7 (sports gear)

- The Market (online “mall”)

Let’s look at how they break down:

The top section shows sales.

Look at the very top line, which is for their core business (The Warehouse).

You can see their sales have barely grown over the last five years – $1.74b to $1.8b, which is about 3.5% and doesn’t even match inflation.

Warehouse Stationery sales have actually gone down over five years.

Noel Leeming and Torpedo7 on the other hand have grown around 39% and 67% respectively, which is decent.

The bottom half shows profit. Everything was up in 2021, The Warehouse actually more than tripled profit for the year. However, keep in mind that The Warehouse had an unusually strong year in 2021 due to Covid lockdowns (Warehouse was an essential service). Otherwise, you can see between 2017 and 2020, numbers are flat or down.

We can also see Torpedo7 made its first profit in 2021, and The Market is loss-making.

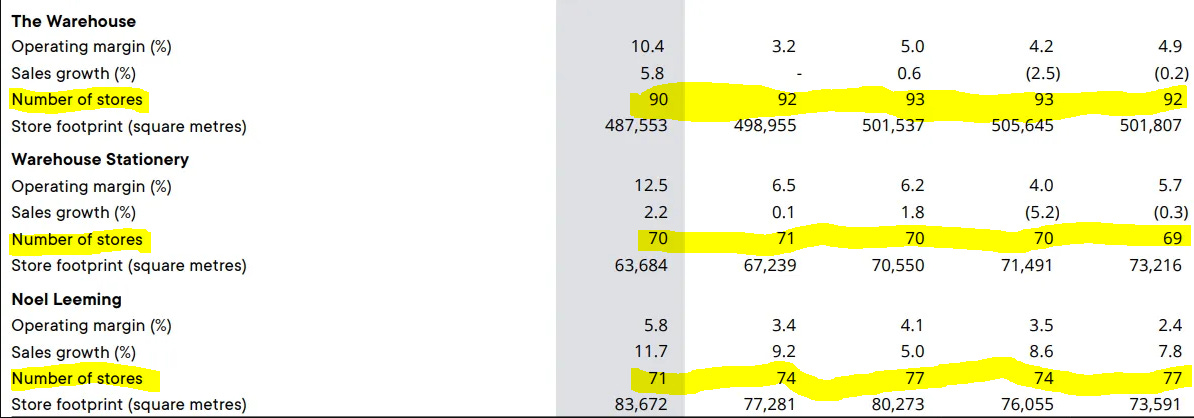

Another helpful metric is store growth. Here are the last five years:

This tells me the obvious reason that sales aren’t increasing – because they’re not opening new stores.

This suggests their three core businesses have reached saturation in New Zealand, i.e. there are not many more malls or towns that don’t already have a Warehouse or Noel Leeming.

If you can’t open new stores, it’s kind of hard to grow.

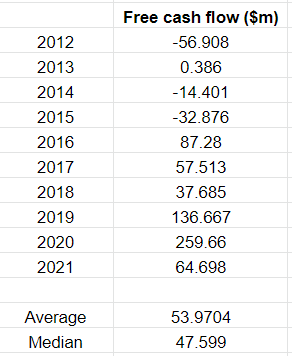

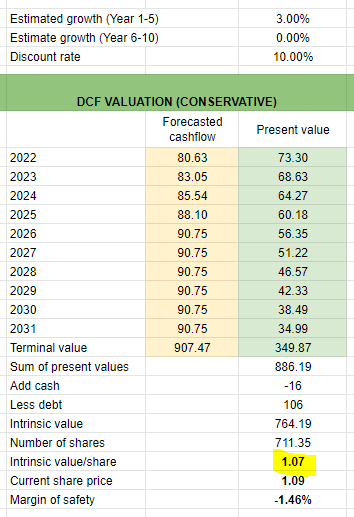

Let’s look at valuation. I use a basic DCF valuation based on past years’ FCF (free cash flow).

The Warehouse is difficult to value because it has very inconsistent FCF (that alone is often enough to pass on an investment, because you need predictable future free cash flows to value anything).

However, the numbers above show us a few things:

Their FCF is improving – it was negative for three out of five years from 2012-2016, but has been positive for all of 2017-2021.

It’s erratic between 2017 and 2021, but we already know that 2020 and 2021 were outliers due to Covid.

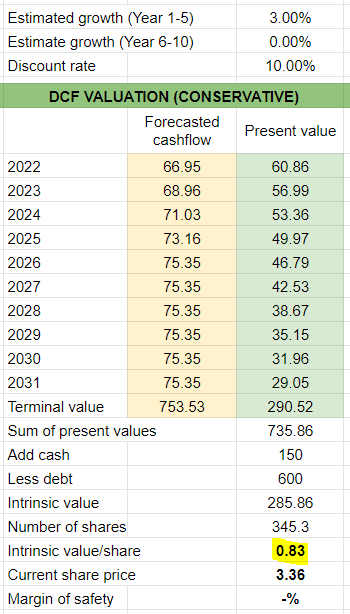

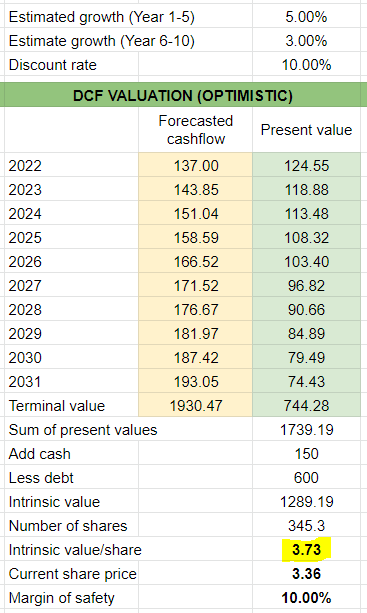

To try and come up with a valuation range, we need to make a few assumptions.

Conservative assumption: Take their latest $65m in free cash flow as their new normal, and we’ll grow approximately 3% per year for Year 1-5, and no growth in Year 6-10.

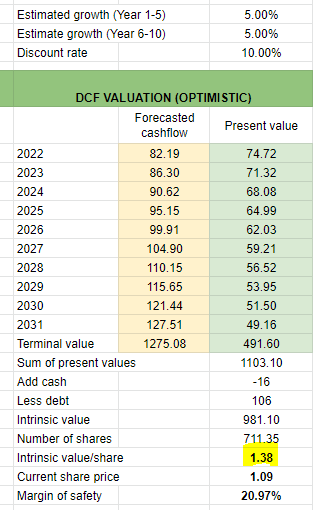

Optimistic assumption: Their 2019 (pre-covid) free cashflow of $137m is their new normal, and we’ll grow approximately 5% in Year 1-5, and 3% in Year 6-10.

Our conservative valuation shows the stock is heavily overvalued, and our optimistic valuation says the stock is trading around 10% under fair value.

Verdict on The Warehouse:

The main issue I see with The Warehouse is they’ve exhausted their avenues for growth. New Zealand is already saturated and they’ve already had one failed Australia expansion.

This is a problem because their margins are so tiny. As a discount retailer this is expected because you’re trying to win customers by having the lowest prices, but the success of this business model relies on volume.

The reason companies like Walmart and Costco are so successful is because even though they might only make 1% or 2% on a sale they move massive volume. Unfortunately, New Zealand is barely the size of a small US city so it’s impossible for The Warehouse to hit the volume needed to catalyse that kind of growth.

The only way I see The Warehouse being a good investment is if it’s massively undervalued by the market – but even on a (very) optimistic model, right now the market has it pretty close to fair value. This one’s an easy pass for me.

Hallenstein Glasson Holdings (HLG)

Hallenstein Glasson Holdings is a clothing retailer that offers mid-range clothing aimed at teens and young adults.

They have two brands – Hallensteins aimed at males, and Glassons aimed at females.

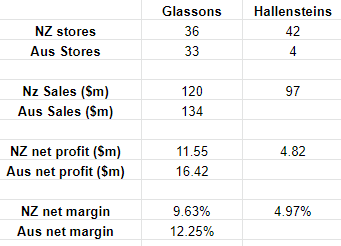

Some numbers:

It’s clear the star of the show is Glassons – they make 85% of the profit and the margins are double that of Hallensteins.

The interesting thing is Hallensteins actually makes 27% of the revenue, but only 15% of the profit. Women’s clothing seems to be much more profitable than men’s, even on a per-item basis, probably because most women are willing to pay more for clothes than men.

Also Hallensteins is almost exclusively NZ based (42 stores in NZ, 4 in Australia). As they’re probably close to saturation in NZ, any growth is likely to come from Australia.

However, the Hallensteins business is far inferior to the Glassons business (Glassons has six less stores than Hallensteins in NZ, but makes more than twice as much profit).

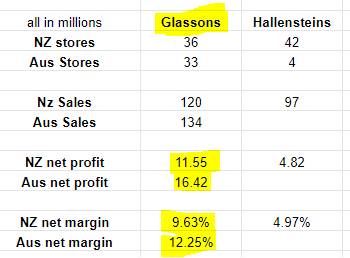

Let’s break down Glassons down a little more:

Glassons Australia has three fewer stores than Glassons NZ, but does $14m more in sales, $5m more in net profit, and achieves 3% higher margins.

Lots of possible reasons for this, including higher incomes in Australia, bigger malls and therefore stores, and higher prices.

In any case, it’s clear the growth for this company depends on their ability to grow in Australia, and it’s going to depend mostly on the Glassons brand.

Let’s look at valuation.

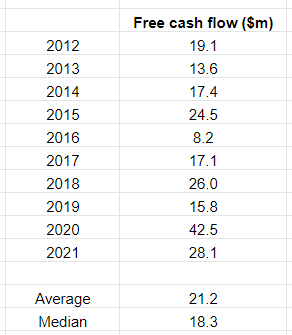

Their free cash flow hasn’t changed much in the last ten years:

This indicates a mature business that probably won’t grow a lot.

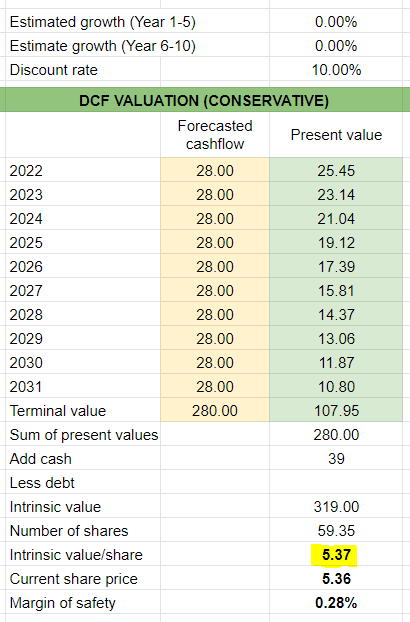

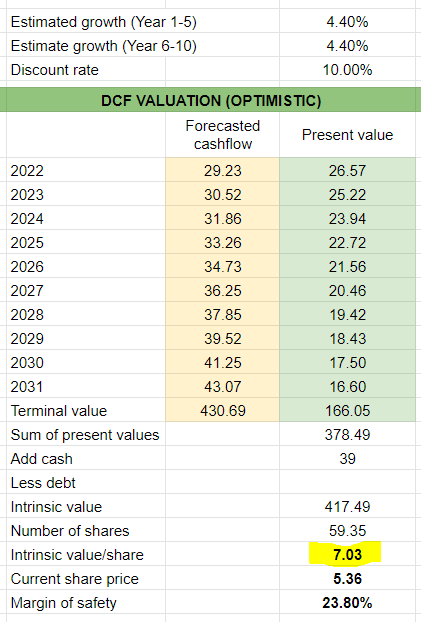

Their free cash flow CAGR over the last 10 years has been 4.4%, so as a conservative estimate I’ll just assume zero growth over the next 10 years, and as an optimistic estimate I’ll assume 4.4% growth for the next 10 years.

Under our optimistic estimate, we have a margin of safety of 24%, which is not quite in my buy zone (I prefer 30% to 50%).

Under our conservative estimate, we’re basically trading at fair value.

Verdict on Hallenstein Glasson:

I’ve always thought HLG was one of the better-managed businesses on the NZX. They are permanently debt-free and always pay out a large reliable dividend, usually around 6% and sometimes as high as 10%. It’s basically a cash cow that churns out low-cost clothes with pretty good marketing and returns a big chunk of cash to shareholders each year.

However, for a zero-growth business I would need a larger margin of safety valuation wise. At a lower price I could be interested, but at current prices it’s a pass.

Michael Hill

Michael Hill is a jewellery brand founded in New Zealand. It currently operates in New Zealand, Australia and Canada.

There is a lot to like about the company on the surface:

- It’s one of the most recognisable brands in the country with a good reputation and is a staple in every major mall and shopping street.

- The Hill family is still involved and owns around 42% of the company.

- Rob Fyfe is the current Chairman with a $2.5m stake and did great things during his time at Air NZ.

- Their loyalty programme Brilliance by Michael Hill has over a million members.

- The balance sheet is a fortress with $99m in cash and no bank debt.

- Very high gross margins (65% at the latest half-year update).

Some numbers:

Some observations:

- Australia is the biggest region by far, with 150 stores, compared with 86 for Canada and 49 for New Zealand.

- Canada is the least profitable on a per store basis, bringing in only $174k EBIT per store, compared to $714k for NZ, and $420k for Australia. This is a big discrepancy; one NZ store brings in more EBIT than four Canadian stores combined.

- Gross margins are mostly equal across all regions.

Some red flags I see on the surface:

- Revenue isn’t growing. If revenue hasn’t grown over five years that’s a problem. Sometimes you’ll have new regions where revenue is growing and established regions which are stable cash cows, but here we don’t have that. All three regions have flat or falling revenue over the last five years.

- EBIT isn’t growing either. You could argue it’s growing very slightly, but not good.

- Store count is decreasing. This is concerning because growth in retail stocks usually comes from expansion – they open stores which make a bunch of profit which they use to open more stores. Retail stocks can’t scale like tech companies, so growth generally is a product of increasing store count or big traction in online sales. We saw this already with The Warehouse and it’s a similar situation here, the difference is Michael Hill operates in three countries and should have growth opportunities but doesn’t seem to be able to capitalise.

The most profitable region by far is New Zealand, bringing in $714k per store per year. More NZ stores would be ideal, but unfortunately the NZ market is saturated – there are only so many malls you can put your stores in – so the store count in NZ hasn’t risen in five years (it’s actually fallen from 52 to 49).

Canada would be the obvious place to grow store count (and they are slowly) but the problem is the Canadian market is far inferior to NZ and Australia. Even if they open 100 new stores in Canada tomorrow, at current numbers they’ll still be making less from Canada than from NZ or Australia.

Just from these numbers, this stock is likely a pass unless the market is offering a price that is so low it’s a no-brainer.

Let’s take a look at valuation.

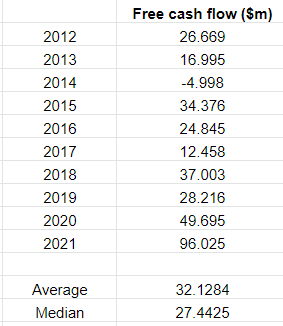

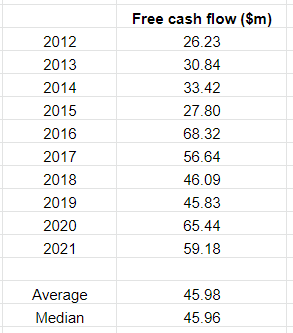

Last ten years of free cash flow:

A few assumptions:

- Free cash flow spiked during Covid, and we can’t know what it will normalise to in the coming years. However, it is a mature business that hasn’t grown much (we can see FCF in 2012 and 2019 was the same). I’ll take the average of $32m as our forecast for Year 1.

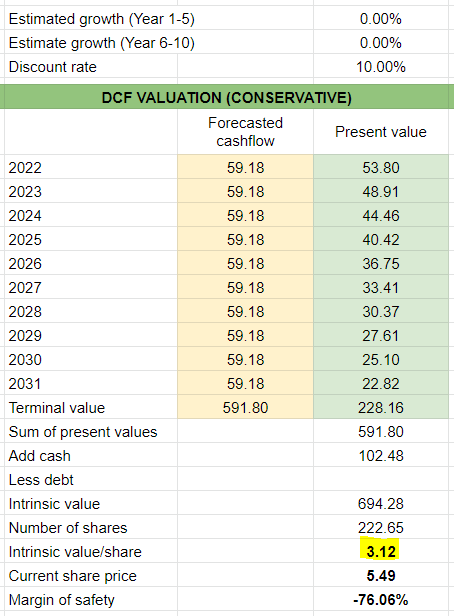

- Conservative forecast is 0% growth for the next 10 years.

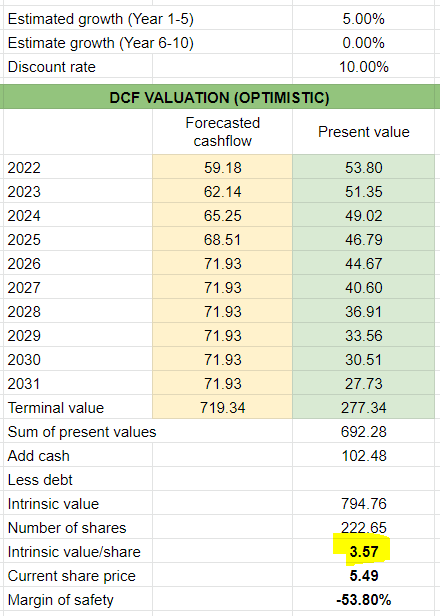

- Optimistic forecast is 5% for Year 1-5 and 0% growth for Year 6-10.

Even at zero forecasted growth, at current prices it’s 30% undervalued. On our optimistic forecast the margin of safety rises to 41%.

Verdict on Michael Hill

One thing that stands out is the strong balance sheet ($99m cash and no debt) so while the cash flows aren’t special the valuation does come out strong because you’re getting $99m of cash for free. Even with zero forecasted growth over 10 years, you’re getting a 30% margin of safety.

However as sales haven’t grown at all over five years, and the NZ market is completely saturated, flat growth is probable and even negative growth is possible.

I don’t think it’s a risky investment, but for them to grow they need massive margin improvement in Canada. Otherwise, the only way I see them growing is via acquisition, which they don’t have a good track record of (they acquired Emma and Roe in the US and divested in 2018 after they couldn’t turn a profit).

It’s a well-managed company and pays a stable dividend, but more likely this will remain a dividend stock with little to no growth. It’s an easy pass for me (at this price). With a 50%+ margin of safety, I’d take another look.

Briscoes Group

Briscoes was founded as a hardware retailer in Dunedin over 150 years ago, in 1862. Its original business was supplying prospectors with shovels, lanterns and tents during the 1860’s gold rush.

Of course, the company has evolved since then, through several recessions and two world wars, but the modern Briscoes you know today really began in 1988. Australian big hitter Rod Duke took over the company and aimed to turn it into New Zealand’s top homeware retailer.

By most measures he succeeded, and with a 77% stake in the company, he is now a NZD billionaire.

Already there is a lot to like in this story. I like companies with long histories as it proves longevity in both culture and profitability. I like CEOs with very large stakes. I like simple businesses that I’ve been a customer of myself and are easy to understand. I like businesses with a brand that is recognisable to everyone in the country (every New Zealander knows the “Briscoes you’ll never buy better” jingle).

What does Briscoes look like today?

They own three distinct brands/businesses:

- Briscoes (homewares)

- Living and Giving (homewares and gifts)

- Rebel Sport (sporting goods)

They also own a 6.77% stake in NZ clothing retailer Kathmandu (KMD.NZ).

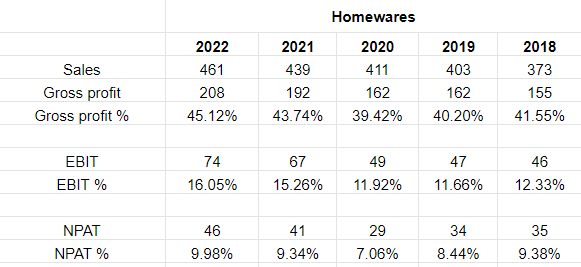

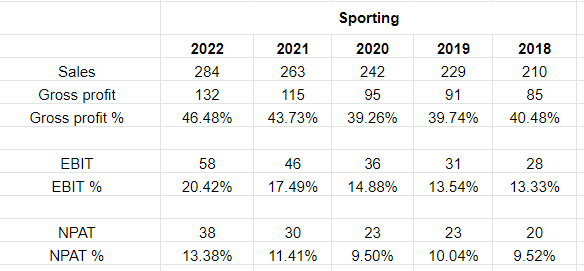

Some numbers:

For a mature business that pays a strong dividend, both of these segments look pretty good.

Sales and profits are growing steadily and the margins are consistent and healthy.

Homewares earns more, but sporting has considerably better margins.

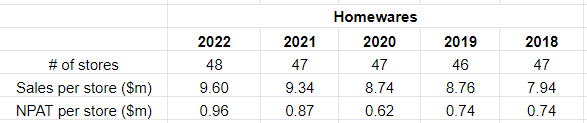

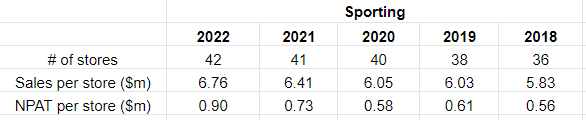

What would help is breaking down numbers per store:

This shows me three things:

- Briscoes store count is flat over five years, while Rebel is still growing (slowly).

- Briscoes makes $960k profit per store per year, while Rebel makes $900k, so stores in both segments bring in about equal amounts of profit. However, Rebel is the more efficient business – each Rebel store does about 30% less in sales than Briscoes stores, but their per-store profits are almost equal.

- Thinking about the NZ retail infrastructure and the way its malls and shopping districts are set up, I would think every mall/park where a Briscoes exists, a Rebel should also exist. There are six more Briscoes than Rebels in the country, meaning there’s still some growing room for Rebel (and maybe even Briscoes too). An additional six Rebel stores at $900k profit per store would add another $5m to the bottom line.

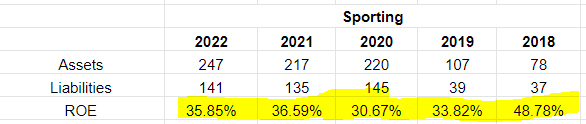

One helpful thing Briscoes Group does is split out the assets and liabilities of each segment. This means we can calculate Return On Equity (approximately) for each business individually:

Of course, there are some assets/liabilities that are unallocated, so the group’s ROE will be slightly lower (it comes in at ~29% overall) but both segments look like strong and efficient businesses.

Let’s look at valuation.

Free cash flow has been mostly flat over the last five years. The good news is it’s also been reasonably consistent within that $45m to $65m range, so it’s not too difficult to get a realistic forecast.

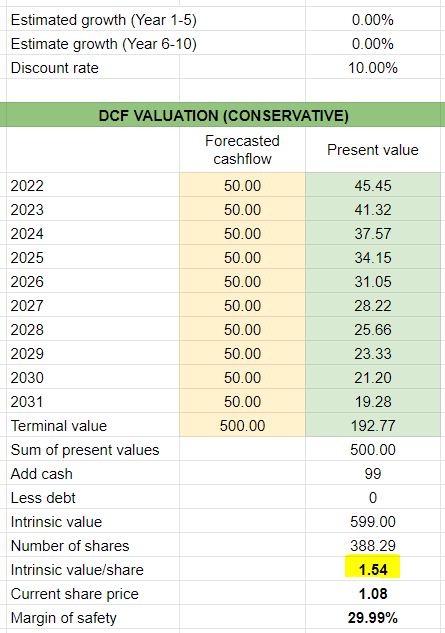

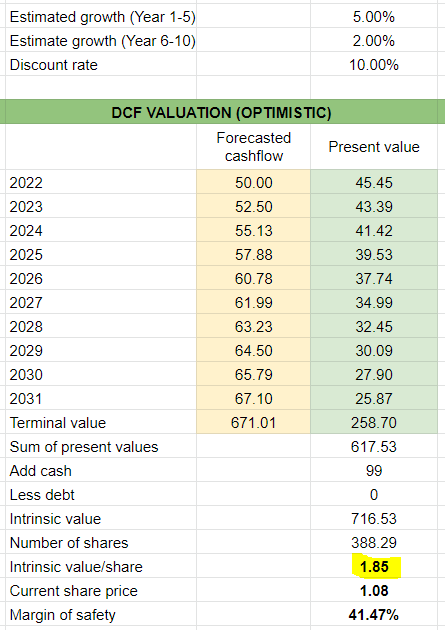

As a conservative estimate, we could assume zero growth over ten years.

As an optimistic estimate, we could assume 5% for years 1-5, and zero growth thereafter.

Even on an optimistic forecast, the market values it way above intrinsic value. By my (rough) calculation, at the current price the market is expecting it to do ~10% growth per year for the next 10 years.

Verdict on Briscoes

I really like the business. It’s sitting on over $100m in cash and run by a great CEO who lives and breathes retail and has for many decades. The dividend is strong. The fact that they’re still growing sales at Briscoes on a same-store basis in such a mature business is a big green tick on how this company is being managed. I don’t often go to Briscoes, but I go to Rebel often and almost never leave the store without a purchase.

Unfortunately, both forecasts show the company is heavily overvalued (a back-of-the-envelope calculation on this would have been obvious – they make around $40m to $60m free cash flow against a market cap of $1.2b – around 20x).

There’s still a lot to investigate but based on these numbers, I’d happily buy this business at the right price (somewhere in the $2.50-$3 range). That’s a long way from the market price and I don’t see it heading that way any time soon. Pass for now (unfortunately).

KMD Brands

KMD Brands began with the Kathmandu brand, which is an outdoor clothing retailer and became a household name in New Zealand before going public in 2009. They acquired US outdoor footwear brand Oboz in 2018 and Australian surf brand Rip Curl in 2019, leading them to rebrand the company to KMD Brands.

Let’s break down what their footprint looks like:

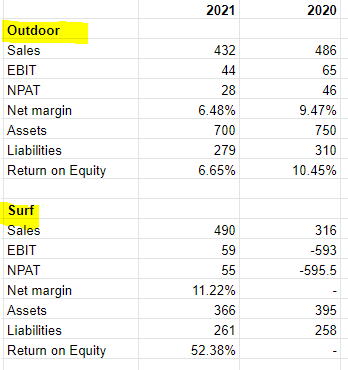

Interestingly Rip Curl is now their biggest brand. It has the most physical stores, the most online stores and the largest wholesale presence.

Kathmandu is second with 160 stores within Aus/NZ, but no licensing revenue and smaller wholesale reach.

Oboz is much smaller and only online and wholesale, with no dedicated stores.

If you break this down by region, you can also see Rip Curl penetrates every continent, whereas Kathmandu is purely an Aus/NZ retail play with a small presence in Europe:

So Rip Curl has the bigger footprint, but does it make more money?

We can figure this out by breaking down their profit numbers by segment, but there are a few limitations:

- Rip Curl was only acquired in 2019, so we only have two years of data under KMD management.

- They don’t separate out Oboz on its own in their reports. Instead, they report an “outdoor” segment, which is Oboz and Kathmandu together, and a “surf” segment, which is Rip Curl.

So what we can do is compare the last two years of data between surf and outdoor.

Revenue for Rip Curl is lower in the 2020 year, likely because they were acquired during that year so it’s only a part year.

We can see in 2021 after a full year of business, it does outearn Oboz and Kathmandu. Margins are also substantially better.

We can also see the return on equity for Rip Curl exceeds that of the outdoor businesses. However, we only have one year of data so no conclusions can be drawn. Since they license stores and draw royalties with the Rip Curl brand, it does make sense.

If you want an idea of the split of revenue between Oboz and Kathmandu, we know that Oboz revenue in 2021 was $78m, so it makes up about 18% of the outdoor segment.

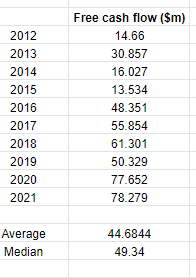

Let’s look at valuation.

As a conservative estimate, let’s assume they’ll grow 3% per year for the next 5 years, and no growth after that:

As an optimistic estimate, let’s say they’ll grow 5% per year for the next 10 years:

Verdict on KMD Brands

For our optimistic estimate, we’ve got a margin of safety of 21% at current prices.

This is not a buy for me, and here’s why:

To start – I do love the brands. I have purchased a lot of Kathmandu gear and Rip Curl gear over the years, as I both travel a lot and surf, and I think both brands are great and valuable. My mother is an enthusiastic hiker and is part of the Kathmandu Summit Club and spends a lot of money there.

However, what I’m seeing on the business side is the Rip Curl and Oboz acquisitions haven’t actually delivered much to the bottom line.

Oboz was acquired in 2018 for US$60m, and Rip Curl was acquired in 2019 for A$350m. That’s almost half a billion NZD in acquisitions yet between 2018 and 2021 their net profit has only grown $12m (from $51m to $63m).

Their free cash flow has only grown $17m (from $61m to $78m).

Of course, Covid had something to do with this, and Rip Curl was a big part of them keeping their numbers up during 2020 and 2021. However, as the success of these acquisitions is still a big question mark, and they don’t look like a bargain at current prices, KMD is an easy pass for me.

So who is the king of the NZ retail sector?

In my opinion…

Nobody.

None of these companies look great to me at current prices.

Now, if I was forced at gunpoint to invest in one, I would probably choose Michael Hill, closely followed by Hallensteins. I’ve actually owned Michael Hill in the past (not anymore) when the market dumped it down to no-brainer prices, and still have a small holding in Hallensteins from some time ago.

Both have very reliable cashflows, strong brands and bulletproof balance sheets, but most importantly are undervalued at current prices. This means they at least have some upside in a good economy. I wouldn’t expect either to multi-bag (or even grow much at all), and I wouldn’t even expect to hold them for the very long term, but the stability and strong dividends would make decent investments that I would sleep easily with.

I’d rank Briscoes third. Based purely on businesses, I actually like Briscoes the most. I like Rod Duke at the helm and how he’s managed to grow it steadily over such a long time, and I think Rebel is a very valuable brand in New Zealand. The reason it’s only my third pick is because of the price. At $1.2b market cap it’s far too expensive for a company generating $60m per year in free cash.

KMD would be fourth, because of the uncertainty of its two new acquisitions, and is probably fully valued right now.

The Warehouse is the easy last pick for me. They barely generate more free cash than Briscoes, Michael Hill or KMD, despite having up to 7x more in sales. A saturated business making 3.5% net margins isn’t something I’m excited to own.

What do you think? Is there any value in the NZ retail sector today? Let me know!

Disclaimer: The numbers and information in this piece are not audited and may be inaccurate. Always do your own research. Investing contains risk and you can lose money. Before you invest your money, you should seek financial advice. This article is not financial advice and I am not your financial advisor. This article is for entertainment purposes only. You are advised to read it under the assumption that I am not very smart and am probably wrong all of the time. Disclosure: Long HLG.