I have a group of friends where we swap business/investment ideas regularly.

If we’re out living life and a good idea comes to mind, we share it and bounce it off each other.

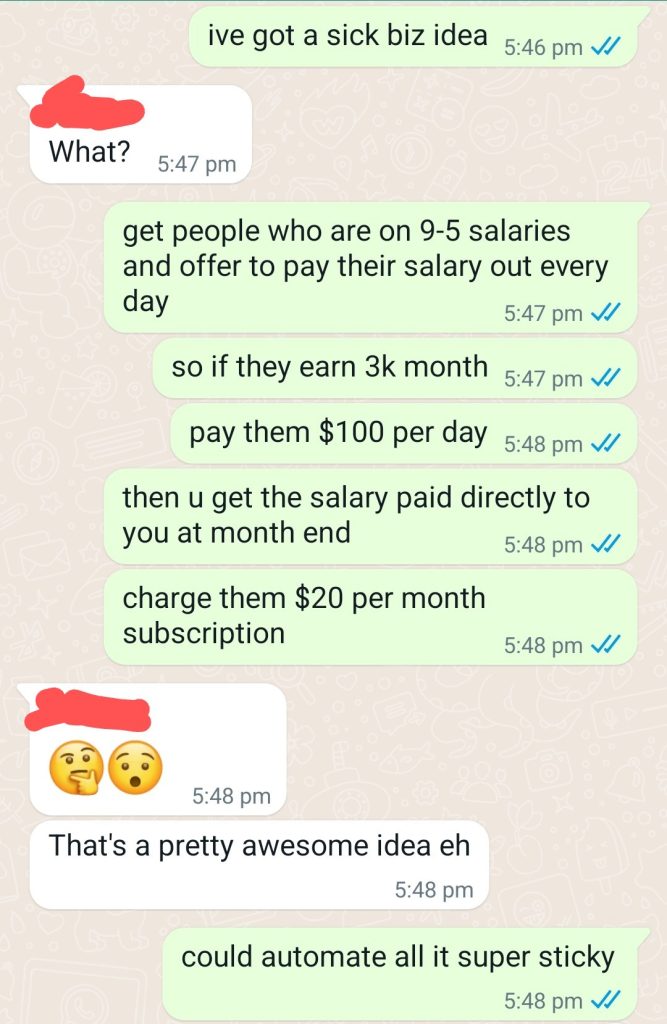

Here’s one of the better ideas I had a couple of years ago:

This was actually an idea I had while reading a blockchain book called The Internet Of Money. They talked about the ability to “stream” income to people. If you were being paid in Bitcoin it would be possible to literally get paid every second (or perhaps more practically, every hour), as everything on blockchain can be safely automated, at very little cost.

Then I thought – even if the banking system can’t pay you every second, it’s still capable of making a payment every day, isn’t it?

Why can’t people get paid every day?

- It would stop people from splurging their paycheck away on payday.

- It would remove the need for high-interest payday loans, and in many cases, credit cards.

- It would help people budget better.

- It would end the issue of people working for weeks and not getting paid.

So many financial issues for NZers would disappear if they didn’t have to wait until payday to access their earnings.

Then last year, an NZX-listed company actually brought that idea to reality.

PayNow was started in partnership with BNZ, allowing employees to access their earned wages or salary whenever they wanted.

How this looks, in reality, is you don’t need to wait until the 15th or 30th to get paid, you can literally choose to get paid at the end of every single working day.

In a world where “payday” has been a thing since probably the beginning of capitalism, I would call that life-changing. Maybe even … revolutionary?

Who Is Paysauce?

The PayNow product was developed in partnership with BNZ by a company called Paysauce.

Interestingly, PayNow isn’t actually the main product, it’s a side feature of their SaaS which deals with all things payroll in NZ.

As an employer, Paysauce manages all your staff’s payroll calculations, including PAYE, ACC, student loan, Kiwisaver, minimum wage requirements, right from the app on your phone.

Simply click a button, Paysauce calculates it all for you and then pays your employee, making sure all your payroll is IRD compliant and everyone gets paid on time.

Paysauce was founded by Asantha Wijeyeratne, who previously developed a similar product called SmartPayroll while working for a tech company called Datacom.

I’m not going to type up the company history here, but you can read their prospectus here and a quick history of SmartPayroll/Paysauce here.

Is Paysauce A Good Investment?

When reading Paysauce’s annual report, it crossed my mind often how many parallels they share with another NZ tech company – Xero.

Xero is a company I invested in back in 2008 and I know their story well as I have followed their journey closely as a shareholder (this story is discussed at length in the Big Baggers lesson in my course Simple Stocks).

Xero listed back in 2007, as a startup making less than $10k in revenue per year.

The Paysauce and Xero products share many similar traits:

- They are necessary/helpful for almost all small businesses.

- Recurring revenue.

- Very sticky.

- SaaS.

- Modern and “nice looking” apps (underrated metric!)

- Incumbents are outdated.

- Disruptive.

Investing in startups is difficult.

Most do not make a profit for years, and much of the analysis is predicting the future without any historical data to base it on.

Currently, Paysauce is unprofitable and has only been listed three years (meaning we only have three years of audited accounts to work with).

However, we can compare them to similar startups that have succeeded in the past, to see if they’re on the same trajectory and are making similar moves.

Xero is an example of a startup that has done everything right, and as a result, at its peak, had returned over 200x (or 20,000%) since it bottomed in 2008.

Is Paysauce on the same track?

Paysauce vs Xero

Interestingly, Paysauce mentions Xero quite often in their prospectus.

One of Xero’s biggest advantages was it was built in the cloud for the cloud, meaning they only needed to develop one single product (instead of a desktop product – usually with multiple versions and updates – and a cloud product).

Paysauce takes the same angle:

Let’s compare Xero in its early stages to Paysauce.

The metrics we use are important.

When evaluating early-stage companies, traditional metrics like PE ratios, dividend yields and FCF are close to meaningless.

Instead, metrics that indicate progress in early-stage SaaS companies are:

- Customer numbers

- Revenue

- Costs

- Lifetime customer value

- Customer acquisition costs

To not over-complicate it – if they can scale customer numbers quickly enough, revenue should follow, and as long as they don’t blowout on costs, they should become (very) profitable in the long run.

Pre-IPO, Paysauce claimed to have accumulated 1,000 customers and annualised subscription revenue of close to $1 million:

Let’s take a look at how they’ve done since listing.

There are a lot of numbers there so let me explain the key ones.

Between 2016 and 2022, Paysauce has:

- Grown subscriber numbers from 200 to 6,000.

- Grown subscription revenue from $9,800 to $3.19 million.

- Increased expenses from $310,000 per year to $4.82 million per year.

The business currently trades on the share market for $39.8 million NZD, which means you would be paying 12.45x sales if you invested today.

Let’s compare this with Xero in their earliest years.

Now we have some context, let’s go through Paysauce’s numbers again.

In the first seven years of listing:

- Paysauce grew subscribers from 200 to 6,000.

- Xero grew subscribers from 204 to 157,000.

- Paysauce grew subscription revenue from $9,800 to $3.19 million.

- Xero grew subscription revenue from $10,000 to $36 million.

- Paysauce increased expenses from $310,000 p.a. to $4.82 million p.a.

- Xero increased expenses from $1.17 million p.a. to $41.7 million p.a.

It’s clear Xero was the superior performer – while they spent (lost) a lot more money, but they grew their customers and revenue exponentially faster, which ultimately drove their share price higher.

However, this doesn’t mean Paysauce is a poor investment.

As Howard Marks says, the most important thing about an investment is how much you pay.

Even the most awfully unprofitable company could be a good investment if it’s cheap enough.

Let’s see how cheap (or not) Paysauce is.

In the final row of each table, we can see Paysauce trades at multiple of 12x sales.

When Xero was at a similar level of revenue as Paysauce is today ($4m per year), Xero was trading at a multiple of 32x sales.

Even when Xero reached over $30m in revenue, it was trading at 26x sales.

Even though Paysauce is not growing as fast as Xero was, and probably never will, you can buy it a lot cheaper than Xero ever was.

This makes sense – Xero and Paysauce as products are not directly comparable. Every single business in the world is a potential Xero customer. Paysauce has a much more targeted market. Xero had much more funding, so could afford to expand much faster. Xero’s product is much larger and requires much more development.

What might add more context is trying to forecast what Paysauce might look like in the future.

Looking at their quarterly reports so far in FY23, they’re making around $1.1m in revenue per quarter, meaning they will probably do around $4.5m for the year (about 40% up on last year) and are adding around 300 customers per quarter (about 20% up on last year).

If we could assume (aka take a wild guess) for the next 5 years, Paysauce will:

- Grow revenue 40% per year (past 7 years has been 162% per year).

- Grow subscribers 20% per year (past 7 years has been 77% per year).

- Keep cost increases to 40% per year (past 7 years has been 60% per year).

- Continue to trade at a 10x sales multiple.

Here’s how that would look:

Subscription revenue would rise to $17 million.

If the market continues to give Paysauce a 10x multiple, that would make them a $172 million dollar company (~4x from today’s price).

Obviously, there are a lot of “ifs” here.

What is the likelihood they keep growing at 40% per year?

What is the likelihood they can sign up 45,000 more customers?

What is the likelihood the market still values them at 10x?

All impossible questions to answer – but putting these questions into the context of probabilities is your job as an investor.

To add a final bit of context, let’s look at a few more companies.

Remember – investing is all about opportunity cost.

It’s helpful to ask yourself, why would I invest in Paysauce instead of … an ETF? A blue chip? Another SaaS company?

Take a look at how Paysauce compares to these household Saas names:

Would you buy Paysauce at 12x sales when you can buy Spotify at 1.4x sales?

There’s no right answer.

They’re companies at very different stages. Spotify will never double revenue in a single year; Paysauce might. Spotify has a much larger target market. And so on.

The verdict is entirely based on what future you see.

My verdict on Paysauce

Personally, I like the company, and I like the product. I like the founding team. I think they will do well.

What I don’t like is the price.

It’s growing too slowly to command a 12x sales multiple.

High multiples are an issue because even if the company indeed does very well, it doesn’t mean the share price will appreciate.

Even though Paysauce was trading as a $100+ million company a few months ago, it might not get there again quickly.

The market is fickle.

I think Paysauce could triple its revenue and still trade at the same price it’s at today.

Especially with other companies trading at historically low prices, it’s not a bet for me.

If the price retracts a little more, I’ll take another look.

Until then, more fish in the sea.

Enjoyed this?

You can learn everything you need to start building your own stock portfolio in my course Simple Stocks!

Perfect for beginners. Start from as little as $1.