Sky recently released their 2023 annual report.

If you’ve read my previous thesis on Sky, you will know I’m a current shareholder and the stock is held both in the public moneybren portfolio and also my personal portfolio.

Basic thesis

The short version of the investment thesis is Sky TV was a business that had been oversold and was trading below fair value, trading well under book value despite remaining cash flow positive and debt-free. Initial write-up here.

The potential bounceback was amplified with new CEO Sophie Maloney, who has since driven an intense cost-cutting campaign, edged Spark Sport out of the market with aggressive bidding for rights, released the new Sky Box and Sky Pod, launched Sky Broadband, reinstated the dividend, sold the Mt Wellington headquarters building and engineered a $70m capital return to shareholders.

With their robust cash flow, I suspected that Sky would probably cash flow their entire market cap within 4-6 years, and as a monopoly, it was reasonable to think their business would continue to endure after that.

2023 results

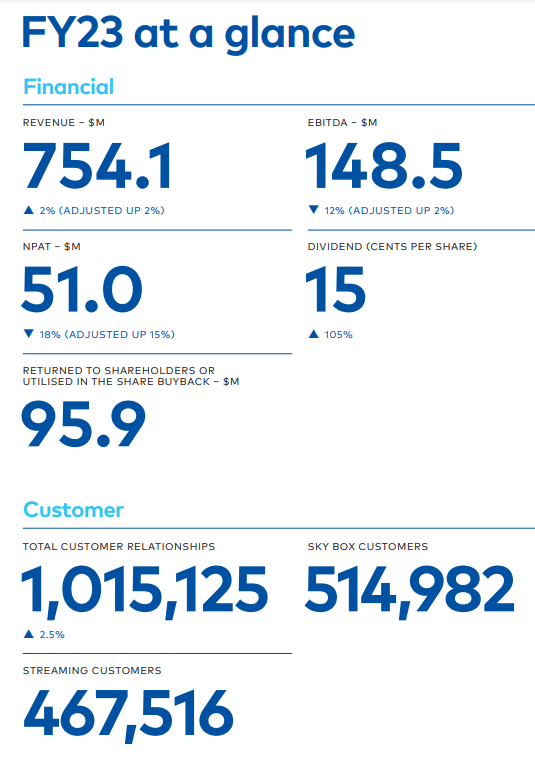

Sky’s results for the year were more or less what I expected, with revenue and profit flat or slightly up. While I expect Sky to grow incrementally, I don’t expect large double-digit growth.

Officially revenue was up 2%, and profit was down 18%, however, last year’s profit is skewed by some one-offs which we’ll get to later. The underlying business has actually grown profit comfortably by about 15%.

Sky also surpassed 1 million customers, split about 45/55 between streaming and Sky Box.

Overall the business continues to generate a reliable cash flow stream, which is central to the investment thesis.

Charlie Munger says the best type of business is one that “gushes cash” once it stops growing. Sky has certainly passed its growth phase and while I wouldn’t say it’s “gushing”, it does continue to generate around $50m in cash flow each year, while selling at a single-digit multiple.

Income Statement

The income statement illustrates how much profit the company made, and how they made it.

First thing you should notice is the top line, showing revenue has increased from $736m last year to $754m this year, an increase of around 2.5%.

However, expenses are also up by about 3%, due to an increase in programming costs (Sky secured a lot of new rights during the year).

While this should lead to flattish profit, profit is actually down on the prior year due to a $16m gain on the sale of a property last year, which obviously is not repeated this year. Take that out, and business profit is up by about $5m, which is about where I expected and am happy with it.

Overall, not too many surprises in the income statement.

Balance Sheet

Nothing surprising in the balance sheet either.

The main change is the cash balance is down by about $80m due to a lot of capital being returned to shareholders this year.

The company returned $70m to shareholders via capital return, $23m via dividend, and $4.5m via share buyback.

In my opinion, this is a sound move. There was talk that Sky was going to use this big lump of cash to acquire some radio stations, which I would’ve shook my head violently at, and certainly would have dumped my stock if it had happened. Thankfully wiser heads prevailed and they distributed this cash to shareholders instead.

You can also see the company has cleared all remaining debts and is now debt-free.

While the company has more goodwill than I would like (much of it will probably end up written off) the balance sheet is stable.

Cash flow

Cash flow is the big daddy of financial statements.

The key metric here is free cash flow – the amount of free cash the company generates from business operations each year, which it is then free to use to give back to shareholders or reinvest in the business.

The components of this are highlighted in yellow: Operational cashflow, minus any capital expenditure, minus any lease payments.

For 2023, free cash flow comes to $46m.

That’s a fair result and I expect this to increase in coming years as their capex requirements normalise.

Looking forward

The Sky team has executed on all fronts since Maloney took the helm and they have very reasonable targets moving forward which I’m confident they can hit.

While everything here looks great – especially the doubling of the dividend, it’s the revenue growth I like the most.

If they can continue to grow the company at 3-4% per year, the thesis should be comfortably intact for an above-average return over the next 3-5 years.

Nothing crazy needs to happen at Sky – just keep the customer churn down and keep collecting monthly subs. Kiwis are never going to stop watching rugby and cricket (there’s nothing else to do in NZ on the weekend!)

If they can keep costs under control, the cash should keep flowing.

While capex at 7-9% of revenue seems high (would also put them at about $60m per year), it still leaves plenty of room to generate free cash.

Sky also has two new revenue streams which are starting to contribute to the bottom line – notably advertising, especially on their free channel Sky Open, and Sky Broadband.

With no debt on the balance sheet and a CEO focused on slashing costs, revenue growth from these additional streams have a good chance of hitting the bottom line.

Verdict on the result

I think the result was mostly in line with expectations.

I don’t expect Sky to grow much in terms of revenue and customers, however, I do expect them to continue to improve cost control and efficiency and to marginally improve revenue each year through their new services, such as Sky Open and Sky Broadband.

Sky TV currently has a market cap of $358m, with $56m in net cash.

If it can maintain its current cashflow level, it should cashflow its entire EV within 5-6 years.

With some improvements, it could potentially do it within 4-5 years.

As it pays 60% to 90% of free cash flow in dividends, you should be receiving much of this cash flow in the hand. The rest should hopefully reflect in the share price.

For a monopoly with great brand recognition, no debt, stable cashflows and a rockstar CEO, I think Sky is one of the better buys on the NZX right now. It might not be the screaming bargain it was when I first called it around $1.70, but even at these prices I’ve added modestly to my position(s).