LULU is now down close to 80% from its highs ($500 to $106 as I write this today).

As you know this is right in my wheelhouse of grabbing great businesses at bargain prices.

The bargain price is there, so let’s see if we’ve got a great business.

First – what’s going on?

Most of the pain started around the time of Trump’s tariffs, with most people assuming Lululemon makes everything in China and all their profit would get tariff’ed away.

Then there were some internal hostilities, with the CEO getting fired (the market liked that) but the new CEO being a former Nike exec (the market didn’t like that). The gist was that Nike has also been punished heavily by the market this year and that all it’s executives are boomer dinosaurs, so bringing over an exec from their was only going to make problem worse.

You also have Chip Wilson, the Lululemon founder and still the biggest shareholder, publicly talking smack about the current board and how useless they all are.

Finally, there is talk that newer brands like Alo and Vuori are eating Lululemon’s lunch and that the brand is dying among the younger gen.

In short, a perfect storm of bad publicity that has nuked the share price of a company that was one a sharemarket darling – LULU listed at $9 per share in 2007, and ran up to a high of $500 in 2021, a more than 50x gain in 15 years.

Let’s look under the hood

I’m not concerned about most of that drama. The only thing I’m concerned about how much money this company makes and will make.

Let’s start with sales.

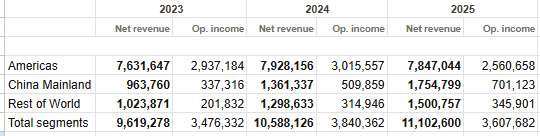

We see a slight drop in Americas sales (that’s USA, Canada Mexico) which means growth in North America might be stalling.

Whether it’s a hiccup or a trend, fashion is always fickle. A big marketing campaign could bring them back to growth or it could flop and lead to further declines. But what we know for sure is USA growth has definitely stopped and is on the downward. A good percentage of that Americas growth is from Mexico, which has gone from 0 to 26 stores in the last 2 years. Take that out, and Americas would be in quite a large decline. We don’t have that data exactly, but a guesstimate at 26 stores is about $400-$500 million sales in Mexico, so US sales are probably down ~6%. Not good.

China is growing like vines and has almost doubled sales in 3 years, which is impressive as China is a huge market for American fashion is we’ve seen with brands like Nike and Hoka. China typically doesn’t reach North American levels but with Americas at nearly $8b and China at $1.7b it’s reasonable to still expect a lot of potential growth there.

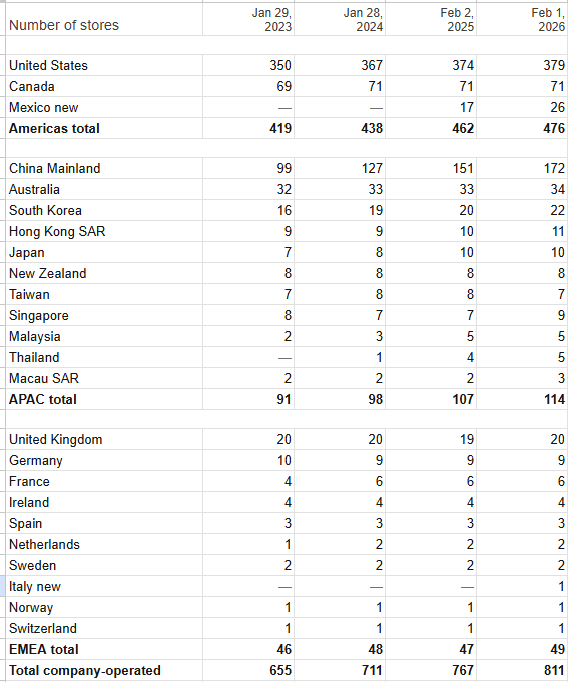

Rest of world is growing slower, but still growing. It’s up 50% over the last 3 years which is strong and not indicative of a dying brand. This mostly consists of Asia Pacific and Europe, where Lulu has a presence but still hasn’t seen the brand become huge like in the US. For example, New Zealand has been stuck at 8 stores for a few years now. But elsewhere growth is still happening, and very few if any countries have had net store closures.

Lulu’s store count for the past 4 years:

So if growth is still happening, why is the company priced like it’s dying?

Well – for the first time in over a decade, the outlook for the current year is sales will be flat at $11.1B. That’s almost identical to last year. So for this year at least, sales growth has come to a stop.

More accurately, sales growth in the Americas is down, and the rest of the world is up, but the balance is a nil change.

Secondly, tariffs are a big hit. The company announced on their latest earnings call that their tariff bill was $275M in 2025, and is expected to be $380M in 2026. That is no joke. It’s about 25% of last year’s profit.

Profit for the year is forecast to be about $1.3B, down on last year’s $1.58B, and the company’s lowest since 2023.

So sales are flat, tariffs and lower sales are leading to a 15% fall in profit, does that justify an 80% drop in share price?

Why I think LULU is resilient

- Tariffs are a very real expense, but they are external and have no bearing on how well a company is run. It’s very different to a company seeing a blowout in expenses because of bad management or cost overruns. The irony is the market punishes tariffs much harder than just an unexplained rise in costs, when one is much more indicative of a loss in company value than the other. A big part of this is Lulu is a Canadian company, so they ship a lot of orders from their Canadian warehouses. There was an $800 “de minimis” exemption on orders coming from Canada, so they can ship their US orders with no need for taxes or duties, but that’s been scrapped under the Trump admin tariff scheme. Now all orders coming from Canada are subject to customs (meaning higher prices) and this is one of the big hits on US sales at the moment. Of course the simple solution would be to just move to distribution centres in the USA, but moving a multi-billion dollar operation takes time. Many of Lulu’s leases run as far as 2040. But the point is – this is a very fixable problem.

- Lulu is stacked with cash. They have about $1.5B in the bank, another $500M in revolving credit and zero debt. They are aggressively buying back stock – they’ve already repurchased $380M this year – and are likely to repurchase up to $1B. This will return a huge amount of value to shareholders. They are also highly profitable, generating about $1B in free cash flow last year, and will do a similar amount this year. The chances of Lulu having solvency problems are practically non-existent.

- The company is experiencing double digit growth internationally. China sales have doubled in the last two years and see no signs of reaching a plateau any time soon. They’re already up 30% this year yoy and is expected to pass $2B in revenue this year. The rest of Asia is also growing nicely with Korea, Japan, Hong Kong, Thailand and Malaysia all seeing net store openings over the last 2 years.

- Lulu has size on its side. It’s got a bulletproof balance sheet and any uncertainty with tariffs or economic weakness can be weathered. Smaller brands don’t have that luxury.

- The product is actually good. You will find almost nobody that has tried Lululemon clothes and doesn’t like them or find them comfortable. They’ve been incredibly sticky with customers until recently, where the CEO last year admitted they were starting to lose their loyal customers finally after being lacklustre on new product releases. But it is much easier to turn around a company with a quality product than one that’s just grown on marketing hype. Lulu does not seem to be that.

- The target consumer is women. It is much easier to make money from women. They buy more products, and spend more when they do. My theory on why Under Armour never managed to grow past the ~$5B sales mark is because the target consumer is male. The marketing was excellent, the product was excellent, they signed good endorsement deals with the right athletes (The Rock, Steph Curry, GSP) but the reality is, men just don’t spend that much on clothes. Most men I know have one gym bag, one pair of gym shoes. They wear the same three singlets on rotation. Most women already have 10x that and still buy more. Under Armour tried (and still tries) for many years to crack the female market, but the brand is just too masculine to reach the tipping point. Lulu is the opposite. The brand is probably too feminine to achieve mainstream adoption by men, but it doesn’t matter. You don’t need the male consumer to make money. Lulu’s core market is young females, and that’s where the money is. If they can get their marketing back on track, I am confident they’ll return to growth in the US.

A lot of talk I see around Lulu is they’re losing market share to the new brands on the block. Brands like Alo and Vuori. I don’t see this being a problem. We see this all the time with brands like AND1, Skechers, FUBU – everyone says they’ll be the next Nike or the next Adidas but brands like this thrive on being niche. Being a chic southern Californian brand like Vuori is the brand. These companies probably do about $500M a year in sales. Lululemon does almost $12B. They might have 50 or 100 stores in a few countries, Lulu has 800 stores across the world. The word on the street is these stores are taking so much of Lulu’s market share that they will grow so big and eat them up, but the reason they are popular now is because they aren’t that big. They’re still the cool alternative brand. The reason Alo is cool is because it isn’t “mainstream” Lululemon. If anything, the fact that Lulu has grown to be “the big brand” is a testament to why its different.

It is outrageously difficult to grow a fashion brand to Lulu’s size. Going from 1B to 10B in sales is not only a logistical nightmare, it’s also a marketing, manufacturing and legal nightmare too. Opening stores in 30 different countries, 30 different currencies, 30 different legal requirements, 30 different tax jurisdictions, 30 different cultures to understand and market to, and succeeding. Not many clothing brands grow past the two or three countries stage, but Lulu has, and they’ve definitively cracked China too, which is the tough one, where they’ll clock $2B in sales there alone this year.

Most people see Lulu sales flattening and think the company’s dying, but there’s a bigger picture they’re missing underneath.

Numbers

Lulu currently trades in the $110 range, for a market cap of $12.4B.

Take off the $1.5B in cash and you get EV of $10.9B.

The company is expected to do $1.2B in net profit and $1B in FCF this year.

That’s 11x cash flow or 9x profit.

Realistically, the days of 30% sales growth are gone. But even if sales and profit stay at this level forever and never grow again, the company would still be a decent value buy today. Over a billion in cash, no debt, and flowing $1B in free cash every year – nothing wrong with that at all!

It’s a good candidate for the “good upside, low downside” play, and those are my favourite.

Disclosure: Long