Walter Schloss.

You may not know the name, but trust me, all the best investors in the world do.

That’s because Schloss was easily one of the greatest investors history has known, achieving a compound return of 15.4% over 45 years.

What’s even more impressive about Schloss is that he did it with a mind-bogglingly simple strategy.

He looked for companies that were trading at a large discount to book value.

This was unique in a time when most investors would base their investments on earnings and PE ratios. But Schloss was adamant that assets were a better indicator:

“Try to buy assets at a discount than to buy earnings. Earnings can change dramatically in a short time. Usually assets change slowly. One has to know much more about a company if one buys earnings.”

So what does it mean to be “buying at a discount to book value”?

Here’s a simple example.

Say you have company XYZ, and they own $100 million of property, and have no debt.

How much would you expect to pay for this company?

Well, logically you could assume you would pay at least $100 million.

Why would the owner of this company sell it to you for less than $100 million, when the net assets are worth $100 million?

However, in the stock market you see this happening all the time.

It is possible that XYZ has $100 million of net assets, but the company is trading on the sharemarket for $50 million.

If you buy shares of this company, essentially you’d be buying $1 of assets for 50 cents.

Now, we know the sharemarket does stupid things every now and then, but usually the stupidity doesn’t last that long. Eventually, it is logical to assume the market will come to its senses and the company will once again start trading for closer to $100 million in the near future.

And of course, when that happens it means your shares will double in value.

Introducing: Arvida Healthcare

Arvida is a retirement village operator based in New Zealand.

I wrote extensively about this industry in a previous analysis, where I compared the four key players: Summerset, Ryman, Oceania and Arvida.

Today, I want to talk specifically about Arvida Group.

As with all retirement home operators, Arvida Group is essentially a home builder.

They build retirement villages (or purchase existing ones), and these villages are used to house retirees.

Their funding model is unique, which I will touch on later, but the business model is basically this:

- Buy land and build a retirement village.

- Lease the units to retirees.

- Use that money to build new villages.

- Rinse and repeat.

The thesis

The thesis is basic:

Arvida Group currently owns around $3.3 billion of property assets (land and housing). This includes land, land for development, and buildings. If you net off their liabilities, it comes to around $1.4 billion of net assets.

As of today, Arvida is trading at $1.04 per share, giving it a market cap of $759 million.

When you buy Arvida, you are buying $1 of property assets for 54 cents.

On top of that, you get the actual property development “business” for free.

Meaning, you are not just buying standalone property at this large discount. You actually get a business on top that is actively developing and selling more housing.

A couple of things to consider here. Buying a company at below book value is not always a slam dunk.

In fact, there’s usually a good reason the company is selling below its asset value.

Reasons can be, they’re caught up in some kind of scandal, their business is losing money, they’re in a dying industry, the assets they hold are overstated and worth much less than they say, they’re being sued and might owe a lot of money soon, and the list goes on.

Specifically with Arvida, I believe the following are important risk factors to investigate before investing:

- We need to ensure the business is not losing money. Even if you’re buying the assets at a discount, it’s worthless if the business is burning millions in cash per year.

- We need to ensure the business is not at risk of becoming obsolete/worthless. Even if you’re buying assets a large discount, it’s still risky if their business is something useless, like fax machines or phone books.

- We need to ensure the business is not at risk of defaulting on debts. If the company is saddled with debt at high rates, then the value of those assets can be chipped away (or repossessed) very quickly.

Let’s go through these one by one.

We need to ensure the business is not losing money

One thing about the retirement sector is their financial accounts are a little difficult to understand if you’re not an accountant, or don’t have a sound understanding of the industry.

There are several reasons:

- Accounting laws require properties to be reported at “market value”. This means net profit figures are almost always skewed by large property revaluation gains during a property bull market. Even if a company is losing $50 million a year, one of its villages might have been “revalued” up by $100 million. This means their accounts will show a $50 million “profit”, even though cashflow wise they’re losing money.

- When retirement operators “sell” one of their apartments or units, they don’t actually sell ownership. They sell a “right to occupy”, also known as an ORA. The way this works is the resident buys the ORA for $500,000, then when they die or move out, they get $400,000 back. Essentially they are purchasing the right to occupy for $100,000, but need to put down a $500,000 “bond”. It is these “bonds” the company uses as funding to buy and develop new villages. What this means is the Cash Flow statement shows a lot of funds coming in as “receipts”, when it’s in fact new debt.

In summary, both the Cash Flow Statement and the Income Statement are misleading to the naked eye. Both show big profits and operational cashflows, when in reality, neither of those is accurate, and in fact can mean the exact opposite.

To figure out if Arvida is actually making money, you need to dig a little deeper and work out how much money they receive is actually revenue they get to keep, what they spend in operational expenses, and how much debt they truly have, which requires selectively picking figures from both the Income Statement and Cash Flow Statement to build an accurate picture.

I have done that for you.

Here are the relevant numbers for Arvida for the last six years.

Now, this paints a very different picture from the Income Statement, which shows them making hundreds of millions in profit each year.

However, that hundreds of millions in profit isn’t actually “wrong”. It’s just taken out of context.

The figures above show a more accurate picture of how much “cash profit” the company makes.

The “management” fee is the portion of the ORA they get to keep. For example, if a resident buys an ORA for $500,000, and Arvida needs to refund $400,000, that $100,000 “profit” is the management fee.

This is the foundation of a retirement operator’s growth, so it’s important that it’s stable and growing.

We can see Arvida is consistently growing its management fees by around 50% per year.

The “care” fees are revenue from care beds, as well as village service fees, such as the weekly management fee, which is a bit like a body corp for the village.

While the care fees bring in most of the revenue, they also bring in most of the expenses. In fact, for most retirement village operators, the care business loses money. So it’s much more important that the management fees are stable and growing versus the care fees.

Finally, the operational expenses and capital expenses are taken directly from the Cash Flow Statement, to get a gauge of how much the business costs to run.

Overall, we can see Arvida comfortably makes a profit each year. These numbers are actually pretty good when it comes to NZ retirement villages. If you read my breakdown of the industry, Ryman and Oceania actually make operational losses.

Finally, if you add in the fair value property gains Arvida has each year, which reached over $150 million in 2022, they are very comfortably profitable.

Now, will these trends change in the coming eighteen months with rising rates and a falling property market?

Yes, possibly.

I believe we may see the market value of its assets fall at some point, but I do not expect to see its asset quantity fall (as in, they should not be selling any assets). It’s also reasonable to expect any downturn in property values should reverse within a few years. Retirement operators tend to own a lot of land, and if there is one asset that has historically always trended upward in the long run, it’s land.

Also worth noting is the thesis here is not that we’re buying a hugely profitable company.

The thesis is we are buying land and property assets for much less than they are worth. When it comes to evaluating the business’s profitability, we’re not so much looking for mega profits, but rather trying to confirm the company is not making large losses (they aren’t).

The one metric to keep a close eye on is the sale of new ORAs. As long as they are consistently selling new ORAs each quarter, they are likely to be well capitalised and able to keep bank debt low. Resales of existing ORAs are great too, but their effect is to maintain the current level of capitalisation rather than improve it. It’s the new ORAs that add to the company float and improve liquidity, which in turn improves the land bank.

We need to ensure their business is not becoming obsolete

The retirement sector serves a very specific need.

As people become older, their children have moved out or overseas, and their health deteriorates, they require more assistance with living.

This includes things like organised exercise, organised healthcare, specific care for specific ailments, assistance on-hand, plus a community to live in and maintain some sort of social network and connection.

The truth is it is not often practical for people in their 70s and 80s to live alone. Retirement villages serve all of these needs at once, and do it at a reasonable price. If an elderly couple sells their home, it is almost always enough to move into a village and live there for the remainder of their lives.

Here is an extract from a report by Jones Lange Lasalle:

There are currently 345,960 New Zealanders over 75 and estimated this will reach 832,810 by 2048. The demand for retirement village units continues to grow as a reflection of this population increase, and an estimated 24,413 new units will be required by 2033.

However, development has commenced on around 12,238 units, leaving a shortfall of 12,306 units. Market challenges including the global pandemic, rising inflation, labour shortages and supply chain constraints continue to put pressure on the industry. And more diversity of ethnicity of occupiers in retirement villages could create further need for new units.

The market continues to be led by the ‘big six’, which have aggressive growth strategies which will help meet demand and benefit the industry as a whole. The aged care market provides a key part of the continuum of care and acts as a diversifier to the income streams of retirement villages when co-located.

This government report from 2020 offers a similar conclusion:

The proportion of people aged 75+ living in retirement villages is now 13.9%, up from 9.5% in 2012. Some regions have higher village residency rates among that age group – in Auckland 18% of people aged 75+ live in retirement villages, in Bay of Plenty 19%, and in Gisborne 17%.

The data covers the year ending 2019 and is taken from 403 villages. Six companies run 42% of villages, with the number of units in those villages accounting for almost 60% of supply. The total number of residents is estimated at 45,000, the population of a city the size of Hastings. 66% of villages include an aged care facility providing about 50% of total aged care beds nationally.

The residency rate is expected to increase by 23,000 people by 2028, to total about 68,000. This would see demand for units increase by an extra 17,700 units, or around 2200 per year.

What’s more, if you live in New Zealand you are probably familiar with the limitations of the public healthcare system. New Zealand’s population is ageing rapidly, and the government already cannot handle public health needs as it is. Not to mention, we haven’t built any major new public hospitals in the last ten years, and there are none in the pipeline.

If you have had surgery scheduled in a public hospital, you will likely have experienced these limitations yourself. Usually, surgeries and operations have long wait times because “there is only one surgeon in the country who can do this operation” or “there is only one machine and it’s booked in Christchurch for the next four months” or some similar bottleneck that prevents people from getting care in a reasonable timeframe.

The reality is, the reason care beds are always full at retirement villages is because government facilities cannot meet demand and never have come close, and it’s not looking likely they will in the future.

There has been some chatter that governments may clamp down on retirement villages due to ORA terms being unfair, or them making too much money, but I (personal opinion) think this is extremely unlikely. The government knows they absolutely need retirement villages and the services they provide, otherwise, the burden of care will fall on the government who admits themselves they simply do not have the capacity to carry that burden.

If anything, I actually believe it’s far more likely the government will end up subsidising the retirement sector to some degree, as their assistance in handling the increasing aged care demand is so essential.

Not only is Arvida’s business not becoming obsolete, it’s actually growing so quickly in demand that the retirement sector cannot keep up.

We need to ensure the business is not at risk of defaulting on debts

Arvida’s debts currently consist of the following:

- $552 million in interest-bearing loans

- $1.48 billion in resident loans (ORAs)

Let’s address the resident loans first.

In short, these are a non-issue.

First, they do not bear interest. Therefore, these loans could sit on the balance sheet indefinitely and stay immune to interest rate risk.

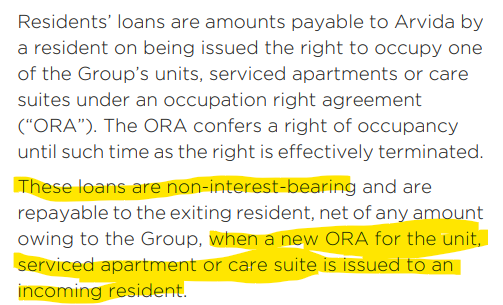

Secondly, the loans do not even need to be repaid from Arvida’s pocket. This is an extract from the annual report:

This means the loan needs to be repaid to an outgoing resident, however, the loan only becomes repayable after the ORA has been resold to someone else.

Here’s how that works in practice:

Jane moves into an Arvida village, buys an ORA for $500,000.

Arvida gets to keep $100,000 as a “management fee”, and must refund the remaining $400,000 when Jane moves out or passes away.

Say Jane finally moves out after five years, and Arvida now owes Jane $400,000.

However, according to the ORA terms, they do not need to pay this until they’ve resold Jane’s apartment to the next resident.

Say it takes them twelve months to resell the ORA – but they finally sell it for $550,000.

Once they receive the $550,000 from the new resident, they give Jane her $400,000, and keep the $150,000 in the bank.

Jane received no interest, and Arvida did not need to take on any debt to repay her. As you can see, there is no liquidity risk posed by the resident loans, and no interest risk either. They simply pay it off as the liquidity becomes available.

However, one risk under this arrangement does exist. There is a risk when it comes to the sale price. If the property market falls significantly, and Arvida is only able to resell the ORA for $300,000, then they can experience some liquidity issues. Since only $300,000 comes in, and they need to pay Jane $400,000, they will need to find that extra liquidity from somewhere (likely from drawing bank debt).

However, as it’s (very) unlikely a large proportion of this debt will become due at once, the risk of this resulting in any kind of default or solvency issue is low.

Now let’s address the interest-bearing debt.

This consists of the following:

- $125m of retail bonds (interest rate 2.87%)

- $430m of various bank loans (interest rates currently between 1.7% and 4.5%)

By any metric, this is a conservative level of gearing ($550 million of interest-bearing debt against $3.3 billion of property, at an average interest rate of ~3%).

Should Arvida need funding (which I don’t expect they will), they have sources available to them – currently $145m of bank facilities are undrawn, plus their accounts are healthy enough that they can reasonably tap the market for capital via a stock issue or bond offer.

Of all the risks facing Arvida, I find debt risk to be the least concerning.

Why Is It So Cheap?

What we’re seeing is punishment across the whole sector by the market.

All four major retirement home operators are currently selling below book:

SUM: 0.88x

OCA: 0.54x

ARV: 0.53x

RYM: 0.77x

The reasons for this are likely multi-pronged, but the strong dip in house prices, plus stubbornly high interest rates forecast for the medium-term, plus inflation, and the possibility of a lengthy recession are all factors.

However, I don’t see any of these as being long-term headwinds, especially for those who are well capitalised, conservatively geared and have high quality assets.

My opinion is SUM is the clear market leader in terms of management and profitability. ARV is a distant second, while RYM and OCA are equal tail-enders. ARV being priced as cheaply as it is, especially in comparison to RYM and OCA is a mispricing and strong buy opportunity.

Summary

As I said earlier, it’s a reasonably simple thesis.

Arvida is in an industry where demand is forecast to grow significantly until at least 2030.

They are conservatively geared with little risk of defaulting on debts.

They have grown profits and shareholders’ equity consistently since going public in 2016.

They currently have a market cap of $759 million, against net assets of $1.42 billion, which consists almost entirely of land and buildings.

Arvida presents an opportunity to buy $1 of land and property assets for 53 cents, on top of which you will get a stable property development/homebuilding business that has grown profits consistently over the last six years.

I expect Arvida to grow to at least book value, and even a healthy 2x to 3x multiple of book value once the rate environment stabilises and the property market recovers.

Resources:

Arvida Annual Reports 2017-2022

Disclaimer: The numbers and information in this piece are not audited and may be inaccurate. Always do your own research. Investing contains risk and you can lose money. Before you invest your money, you should seek financial advice. This article is not financial advice and I am not your financial advisor. This article is for entertainment purposes only. You are advised to read it under the assumption that I am not very smart and am probably wrong all of the time. Disclosure: Long ARV.

Good article.

What about all the share dilution?

Dilution is mostly an issue when staff and executives are being paid an exuberant amount of share-based compensation. Arvida’s dilution is mostly from capital raises – this is only an issue if they raise at low prices, and/or you don’t participate in the raise. From memory their last two big capital raises were at prices higher than the current price, meaning if you buy today, you’re actually benefitting.

How do you think the sector and Arvida is looking at the moment? They've survived a buy out and some negative publicity around that. Now what? They had a significant cash burn and debt expansion in the first half of FY24…

Sales are up and float keeps growing. Thesis still strong for me.